Stock Markets Lost Step After an Epic Rebound. More Trouble May Be Ahead

Stock Markets Lost Step After an Epic Rebound. More Trouble May Be Ahead

By:Ilya Spivak

Investors are looking to U.S. consumers for direction as swaying Fed rate cut bets echo blistering volatility

- U.S. inflation data adds to evidence of an incoming economic downturn.

- Fed rate cut speculation resets to baseline as panic-driven pricing eases.

- Stocks may fall if U.S. consumer sentiment data seems to delay stimulus.

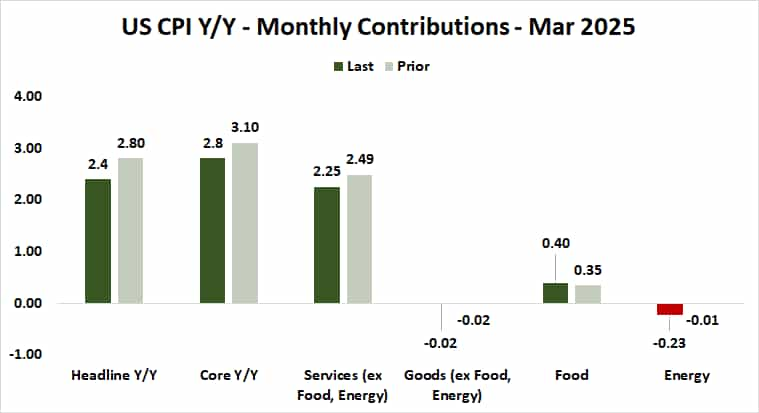

U.S. inflation slowed more sharply than expected in March. The headline consumer price index (CPI) grew 2.4% year-on-year, marking the weakest reading in six months. The core rate excluding volatile food and energy prices – a focal point for Federal Reserve officials – fell to 2.8% year-on-year, the lowest since March 2021.

Moreover, weaker price pressure in the core services category led the way downward. While the space remains the overwhelming growth center for the U.S. economy – contributing 2.25 percentage points (ppt) of the overall headline figure – it saw the biggest disinflationary impulse at -0.24ppt.

Fed rate cut speculation cools despite U.S. inflation slowdown

The data suggests that last month, the upward pull of services demand on prices was at its weakest since December 2021. This at a time when the goods side of the ledger seems to be at a standstill appears to imply that overall economic growth is briskly decelerating. That echoes recessionary signaling in inflation expectations priced into the bond market.

Nevertheless, Fed Funds interest rate futures moved to cut back scope for rate cuts. They now anticipate 104 basis points (bps) in stimulus through the end of 2026, down from 134bps at the start of the week. That amounts to erasing one standard-sized 25bps cut from the baseline.

That broadly lines up with the U.S. central bank’s own forecast. However, the markets envision faster delivery than officials. They’ve priced in 84bps in cuts this year, implying a recession-minded urgency in the projected delivery timeline. The Fed has penciled in 50bps apiece this year and in 2026.

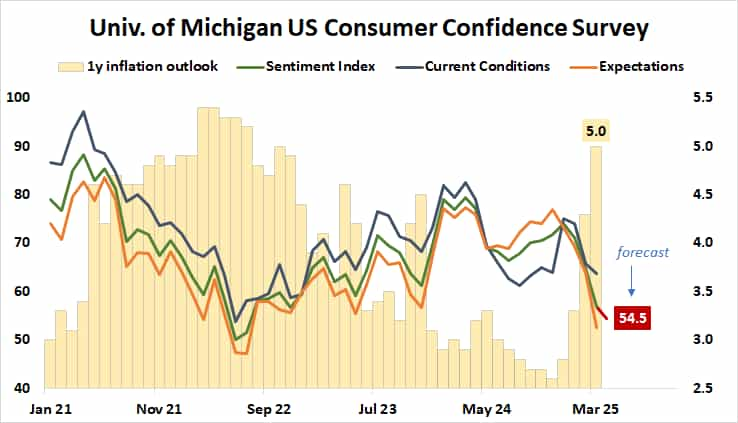

U.S. consumer confidence data next in focus for the markets

The spotlight now turns to U.S. consumer confidence data from the University of Michigan (UofM). It seems hardly surprising that a gloomier sentiment reading is expected. The topline tracker, which will take in an assessment of current conditions and the outlook for what’s next, is expected to slide to the lowest level since July 2022.

Polling data aggregated by RealClearPolitics shows President Trump losing ground with voters in April, so weaker consumer confidence is probably a given. However, the trend in survey respondents’ one-year expectations for inflation might well be a more potent indicator than the sentiment gauge itself.

Worries about the impact of tariffs drove bets on the growth of prices to a blistering 5% in March, the highest since October 2022 and within a hair of the post-COVID high at 5.4%, recorded exactly three years ago. At that time however, observed inflation was hovering near 8%, making the outlook now appear more sentiment-driven by comparison.

On balance, this suggests it probably has not had reason to diminish, nor get have a lot of headroom for an upward surge. This may serve to validate the latest pivot in Fed rate cut expectations, implying a slower onramp for stimulus in the near term as officials weigh competing risks. Stock markets are unlikely to be pleased.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.