Interest Rates Are on the Move in the World's Top Three Economies. Now What?

Interest Rates Are on the Move in the World's Top Three Economies. Now What?

By:Ilya Spivak

Investors await U.S. CPI, the ECB rate decision and China stimulus

- Bonds may rise as the dollar falls if expectations for U.S. inflation data are as realized.

- The euro might rise if the ECB chooses not to dial up a dovish policy guidance.

- Chinese trade data may prove just steady enough to mollify hopeful markets.

Financial markets marked time across major assets last week. The tech-oriented Nasdaq 100 was a lone standout on Wall Street, surging to a new record high with a weekly rise of over 3%. The catch-all S&P 500 put in a comparatively modest rise of 0.8%. Gold and crude oil inched slightly lower, bonds tiptoed higher and the U.S. dollar stalled.

Against this backdrop, here are the key macro waypoints to consider in the days ahead.

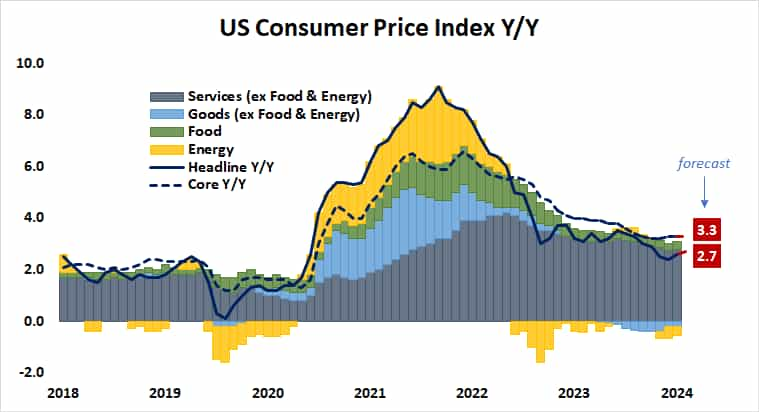

U.S. consumer price index (CPI) data

The Bureau of Labor Statistics (BLS) will report inflation quickened in the U.S. last month, according to economists’ forecasts. The headline consumer price index (CPI) is expected to have grown at 2.7% year-on-year, the fastest since July. The core measure excluding volatile food and energy prices is seen at 3.3% for a third month straight.

On balance, the release is unlikely to dissuade the Federal Reserve from another interest rate cut at this month’s policy meeting. The probability of a 25-basis-point (bps) reduction is currently priced at a commanding 86%. Fed officials have stressed the need to look through near-term data volatility, and a large majority seem to favor easing this month.

Meanwhile, U.S. economic data outcomes have continued to cool relative to baseline expectations, according to Citigroup. If that yields results broadly close to forecasts, the markets might take them as permission to continue the speculative unwinding of the two-month-long reflation trade playing out over the past three weeks.

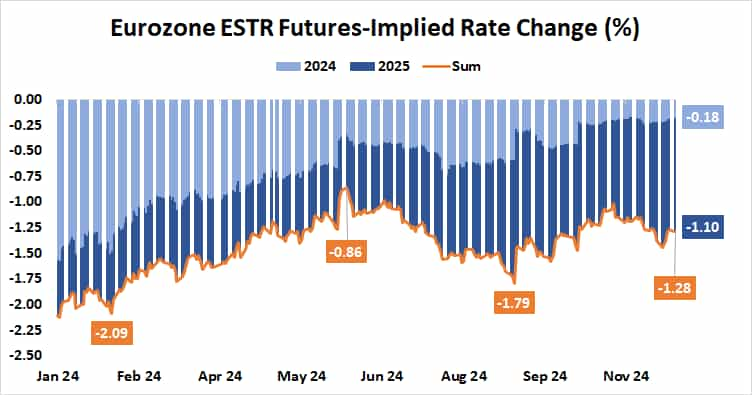

European Central Bank (ECB) interest rate decision

The ECB is widely expected to cut its target deposit interest rate by another 25bps to 3% at this week’s monetary policy meeting. The priced-in probability of the move stands at close to 72%, based on benchmark ESTR rate futures. That is likely to shift traders’ focus on the guidance about what is likely ahead in 2025.

As it stands, the markets anticipate a further 100bps in rate cuts next year. Soggy economic growth readings over recent months might argue for dovish guidance. However, rising inflation expectations implied in German bond yields warn against overreach. If these crosscurrents distill to status-quo results, the euro may rally with relief.

Chinese trade data

Export growth slowed while imports remained near standstill in China last month, according to numbers expected from China’s General Administration of Customs (GAC) this week. Inflation figures published over the weekend showed consumer prices disappointed yet again while wholesale costs continued to fall.

The world’s second-largest economy is in dire straits after six consecutive quarters of deflation, reflecting a near-total absence of demand. A meeting of the policy-steering Politburo—a 24-member committee including President Xi Jinping—fueled hopes for more aggressive stimulus over the weekend, pledging a “more proactive” fiscal policy.

Whether such hopes bear fruit this time after many similar promises came and went without concrete action remains to be seen. However, a broader improvement in Chinese data outcomes relative to forecasts recently might mean that markets are willing to give Beijing officialdom the benefit of the doubt.

With that in mind, proxy assets for China’s economic growth—like copper and the Australian dollar—may find their way higher as long as trade figures are not terribly disappointing.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.