U.S. CPI Inflation, ECB Interest Rate Decision: Macro Week Ahead

U.S. CPI Inflation, ECB Interest Rate Decision: Macro Week Ahead

By:Ilya Spivak

Stocks may fall for a second week as cooling U.S. economic data and a defensive ECB feed global recession fears

- U.S. CPI inflation data might spook stocks, despite a Fed policy standstill.

- The Euro could fall if the ECB cools expectations of another interest rate hike this year.

- Retail sales, consumer confidence data may show U.S. consumers under pressure.

Stocks fell last week, with rising crude oil prices appearing to spook investors into thinking that costlier energy will make for stickier inflation and higher-for-longer interest rates. Bond yields rose and prices fell across global markets. The US dollar joined the rally, while non-interest-bearing gold declined.

Here are the key macro waypoints likely to drive price action in the week ahead:

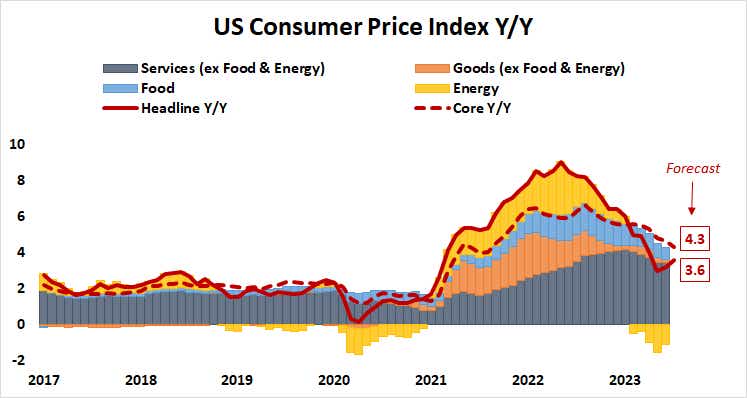

U.S. consumer price index (CPI) inflation

U.S. inflation is expected to have quickened in August, with the consumer price index (CPI) benchmark rising to 3.6% year-on-year. However, stripping out volatile food and energy prices is projected to produce a core rate of 4.3%, the lowest since September 2021.

This suggests the Fed is seen making continued progress toward relieving price pressure in the service sector, the main inflationary culprit in policymakers’ crosshairs. That would endorse a priced-in policy outlook envisioning no more interest rate hikes, with cuts due to begin by June 2024.

It might also spook the markets, implying that the long-awaited economic pain meant to unstick stubborn inflation in the labor market has arrived. That portends job losses and reduced spending, a toxic mix for an economy overwhelmingly driven by consumption. Stocks may wobble while the U.S. dollar, the Japanese yen and Treasury bonds advance.

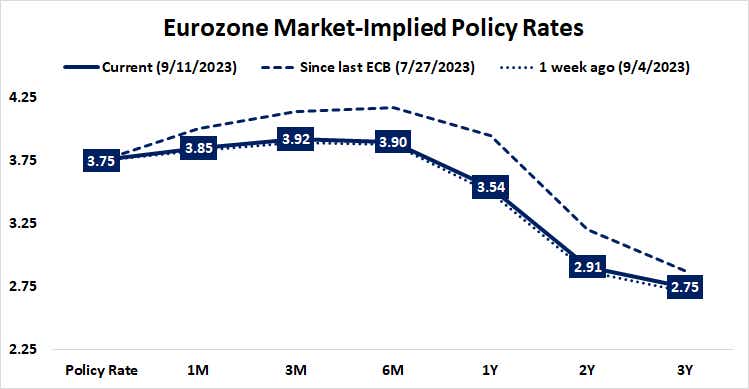

The European Central Bank (ECB) interest rate decision

The European Central Bank (ECB) is expected to keep its target interest rate unchanged at 3.75% this month. Still, the markets assign a non-negligible 40% change of a 25-basis-point (bps) rate hike. The likelihood of such an increase before the calendar turns to 2024 is an even more commanding 75%.

ECB President Christine Lagarde and company have clearly toned down some of the ultra-hawkish rhetoric from earlier in the year as the economy slips toward recession, but with inflation at 5.3%, the market still see more that needs to be done to put the central bank’s 2% objective within reach.

That might be starting to look needlessly aggressive for enough of the ECB Governing Council to put a lid on further rate hikes. In fact, officials may have limited agency to bring down goods-driven inflation lingering in the Eurozone. If rhetoric coming out of this week’s conclave signals a pivot toward wait-and-see mode, the euro may decline.

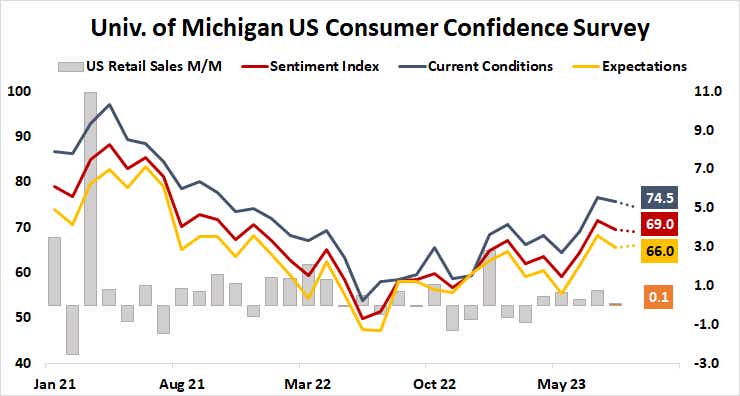

U.S. retail sales and University of Michigan (UofM) consumer confidence

With CPI in the rear-view mirror, Fed-watchers will turn their attention to retail sales data as well as the consumer confidence survey from the University of Michigan (UofM). Receipts are seen rising 0.1% in August, marking the slowest increase since March. The headline sentiment index is expected to fall for a second consecutive month.

The markets are keenly focused on how much pain the Fed needs to inflict on the economy to judge that it has put inflation on a path toward the target 2%. The squeeze has been moderate at best so far. Data showing consumers are finally starting to buckle may put global recession risk in sharp relief, hurting risk appetite.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.