The Truth About Option Premium: Stock Price vs. IV

The Truth About Option Premium: Stock Price vs. IV

By:Kai Zeng

Implied volatility is often more critical to option prices than the volatility of the underlying stock prices

Option sellers are constantly on the hunt for strategies that allow them to capitalize on higher premiums. A fundamental understanding of how the price of the underlying asset and implied volatility (IV) influence option values is crucial for traders who sell naked options.

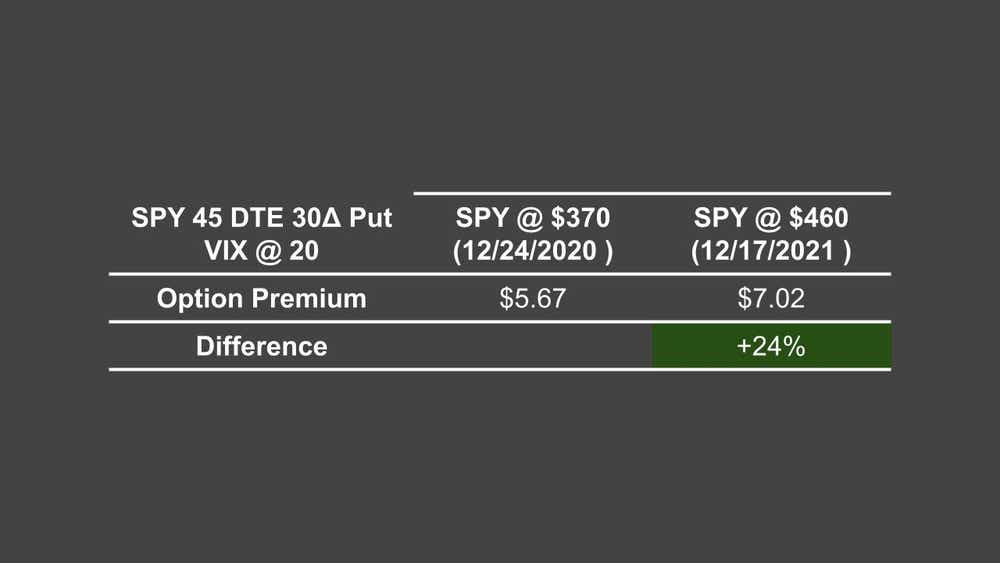

For instance, let's consider the S&P 500 ETF Trust (SPY). With IV held constant at 20%, a $100 increase in the SPY can lead to a 24% rise in the option's price. This demonstrates the significant impact that movements in the underlying asset's price can have on option premiums.

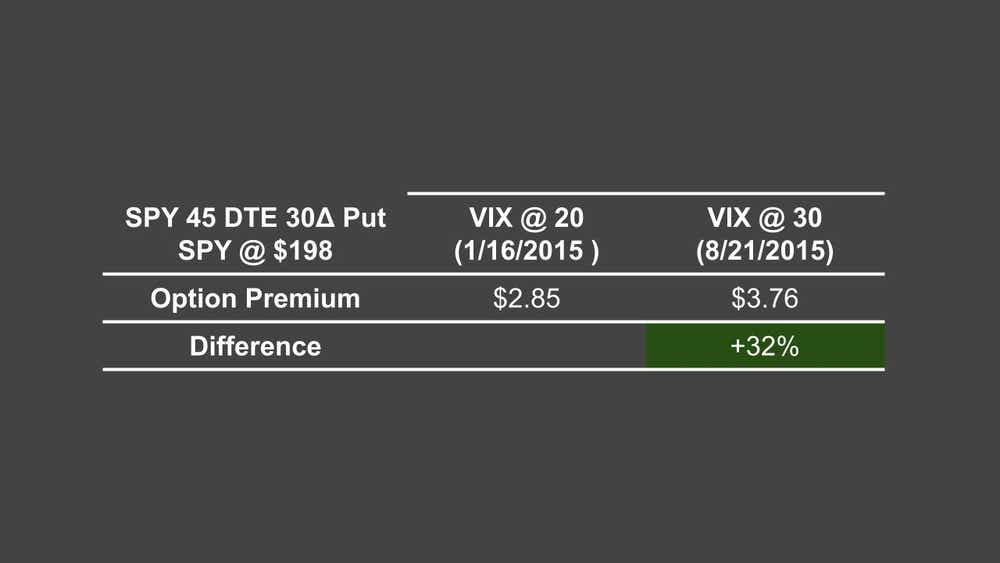

However, when we shift our focus to IV, the effect appears to be even more pronounced. Keeping SPY's price constant, a 10-point increase in SPY's IV could cause the option's price to surge by 32%. This highlights the sensitivity of option prices to fluctuations in IV and underscores the potential for IV to play a more dominant role than even substantial price movements in the underlying asset.

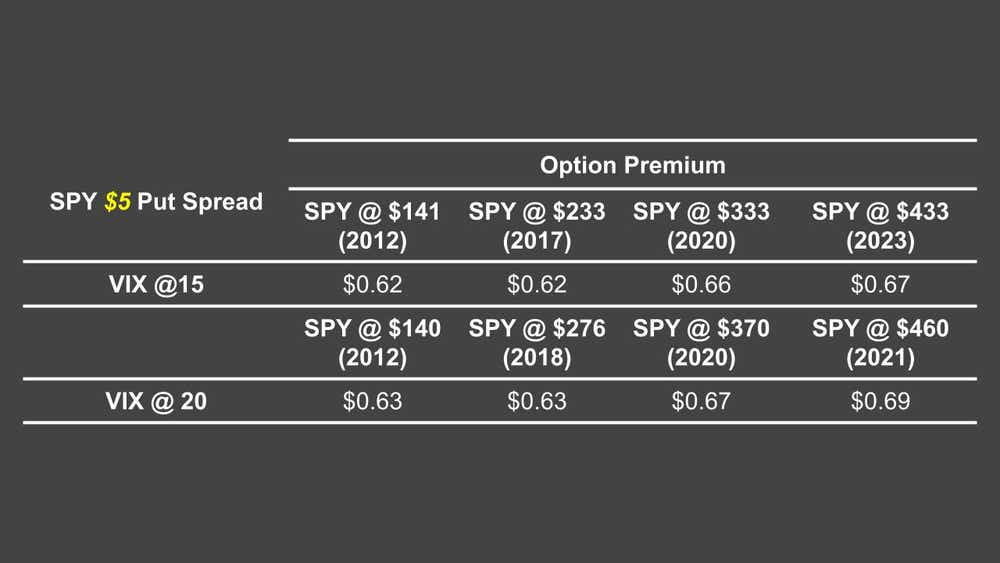

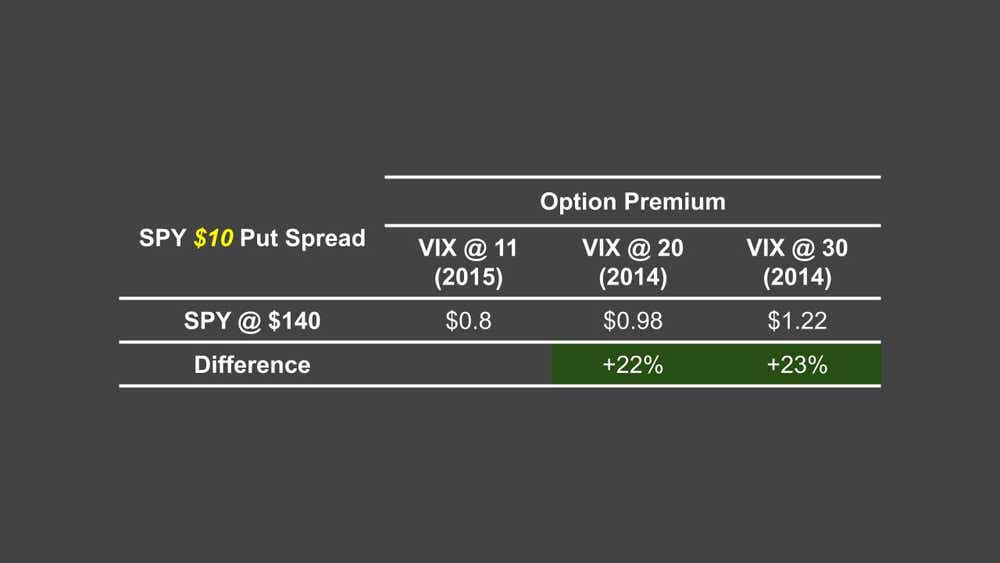

The relationship between price changes, IV, and option premiums extends to risk-defined strategies like put/call spreads and iron condors with fixed wings. For example, in a test conducted with a 45-day-to-expiration (DTE) SPY put spread, by selling 20-delta puts with $5 and $10 widths, the findings were informative. An increase in IV or a rise in the stock price resulted in a minimal change in option premium for a relatively narrower spread like $5-wide spread.

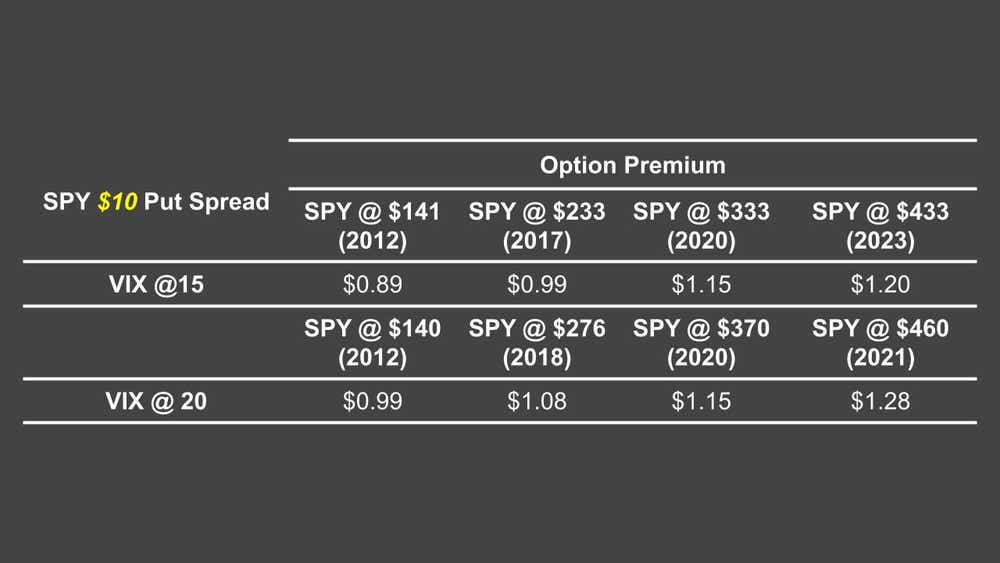

In contrast, the increase in premiums for $10 wide spreads was more significant as stock prices and IV levels increased. But the impact remained relatively modest at approximately 15% for every $100 movement in stock price.

While a $100 change in underlying price may not occur frequently, implied volatility can jump by 10% in a single day in the event of a significant drop in the underlying price.

For instance, in the case of SPY, a 10% increase in VIX could lead to a 22% increase in the premium for a $10 wide put spread - a much larger impact than the change in underlying price alone.

The takeaway for traders is multifaceted.

First, increases in the underlying price and IV typically lead to an increase in the premium of static spreads. Second, the impact of changes in stock price or IV is more pronounced on wider spreads. Lastly, and perhaps most importantly, IV's inherent volatility often makes it a more critical factor in affecting option prices than the volatility of the underlying stock price.

Kai Zeng, director of the research team and head of Chinese content at tastylive, has 20 years of experience in markets and derivatives trading. He cohosts several live shows, including From Theory to Practice and Building Blocks. @kai_zeng1

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.