S&P 500 Futures Sustain Gains After Reports on Retail Sales and Producer Prices

S&P 500 Futures Sustain Gains After Reports on Retail Sales and Producer Prices

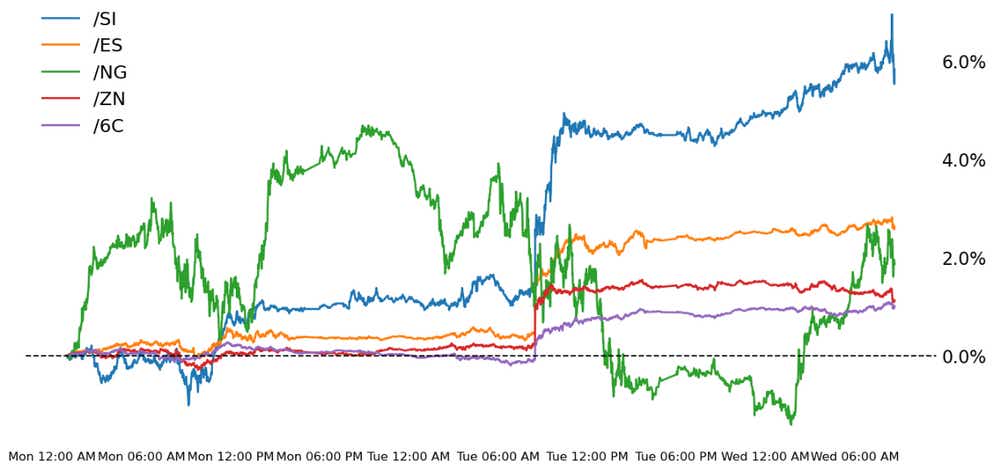

Also, 10-year T-note, silver, natural gas and Canadian dollar futures

- S&P 500 E-mini futures (/ES): +0.35%

- 10-year T-note futures (/ZN): -0.37%

- Silver futures (/SI): +1.42%

- Natural gas futures (/NG): +3.19%

- Canadian dollar futures (/6C): +0.12%

Markets are taking a collective deep breath this morning following yesterday’s astounding performance by both stocks and bonds after the October U.S. inflation report. A weaker than expected October U.S. producer price index, pointing to more disinflation in the pipeline, initially pushed equities higher earlier, but a stronger than anticipated October U.S. retail sales report has cooled off animal spirits—for now. Elsewhere, all eyes are on the Xi-Biden summit in San Francisco, while the House of Representatives has passed spending bills to prevent a government shutdown.

Symbol: Equities | Daily Change |

/ESZ3 | +0.35% |

/NQZ3 | +0.52% |

/RTYZ3 | +0.30% |

/YMZ3 | +0.24% |

Equity index futures are modestly higher this morning—though off of their highs—with all four majors holding in positive territory. The Nasdaq 100 (/NQZ3) is taking the lead thus far, though yesterday’s champion, the Russell 2000 (/RTYZ3), is not too far behind. A slew of earnings reports focused on consumers suggest the U.S. economy remains in solid shape, though there may be some inklings of slowing consumption as the fourth quarter marches forward.

Strategy: (44DTE, ATM) | Strikes | POP | Max Profit | Max Loss |

Iron Condor | Long 4520 p Short 4530 p Short 4620 c Long 4630 c | 18% | +375 | -125 |

Long Strangle | Long 4520 p Long 4630 c | 50% | x | -5112.50 |

Short Put Vertical | Long 4520 p Short 4530 p | 62% | +162.50 | -337.50 |

Symbol: Bonds | Daily Change |

/ZTZ3 | -0.11% |

/ZFZ3 | -0.26% |

/ZNZ3 | -0.37% |

/ZBZ3 | -0.62% |

/UBZ3 | -0.76% |

Bonds are taking a modest step backward this morning after surging across the curve on yesterday. Although Federal Reserve rate hike odds remain markedly depressed—a 0% chance of a 25-basis-point (bps) rate hike at either the December 2023 or January 2024 meetings—yields have pushed higher following the October U.S. retail sales report. The long-end of the curve (10s (/ZNZ3), 30s (/ZBZ3), and ultras (/UBZ3)) remains the focal point, mainly because implied volatility remains persistently elevated.

Strategy (37DTE, ATM) | Strikes | POP | Max Profit | Max Loss |

Iron Condor | Long 106 p Short 106.5 p Short 111.5 c Long 112 c | 63% | +140.63 | -359.38 |

Long Strangle | Long 106 p Long 112 c | 25% | x | -390.63 |

Short Put Vertical | Long 106 p Short 106.5 p | 85% | +78.13 | -421.88 |

Symbol: Metals | Daily Change |

/GCZ3 | +0.19% |

/SIZ3 | +1.42% |

/HGZ3 | +0.45% |

Metals remain on the upswing following yesterday’s positive response to the October U.S. consumer price index. Silver (/SIZ3) has catapulted higher this week, holding onto a gain of over 5% thus far. Copper prices (/HGZ3) are also inching up following a slate of mixed but mostly better than expected Chinese data overnight, which showed industrial output and retail sales were improving above forecasts. Additionally, the Chinese government announced a 1 trillion yuan package to help support the flailing property market.

Strategy (41DTE, ATM) | Strikes | POP | Max Profit | Max Loss |

Iron Condor | Long 23.4 p Short 23.5 p Short 24 c Long 24.1 c | 13% | +430 | -70 |

Long Strangle | Long 23.4 p Long 24.1 c | 46% | x | -6055 |

Short Put Vertical | Long 23.4 p Short 23.5 p | 57% | +235 | -265 |

Symbol: Energy | Daily Change |

/CLZ3 | -0.84% |

/HOZ3 | -0.44% |

/NGZ3 | +3.19% |

/RBZ3 | -1.66% |

Energy markets continue to stumble, the only major group not to enjoy the benefits of yesterday’s jubilance in global markets. Yesterday, the American Petroleum Institute (API) reported a 1.335 million barrel build in crude oil (/CLZ3) inventories for the week ending Nov. 10, just below forecasts of a 1.4 million barrel build. The U.S. Energy Information Administration will release its weekly inventories report today.

Strategy (41DTE, ATM) | Strikes | POP | Max Profit | Max Loss |

Iron Condor | Long 3.1 p Short 3.15 p Short 3.65 c Long 3.7 c | 27% | +360 | -140 |

Long Strangle | Long 3.1 p Long 3.7 c | 41% | x | -3800 |

Short Put Vertical | Long 3.1 p Short 3.15 p | 59% | +220 | -280 |

Symbol: FX | Daily Change |

/6AZ3 | -0.02% |

/6BZ3 | -0.47% |

/6CZ3 | +0.12% |

/6EZ3 | -0.25% |

/6JZ3 | -0.30% |

While the U.S. dollar experienced one of its worst days of 2023 yesterday, another currency was conspicuously sluggish: the Canadian dollar (/6CZ3). There may be a bit of catchup in play today because the loonie—as Canadians call the country’s one-dollar coin—is staging a minor rally while all other majors are pulling back vs. the greenback. Nevertheless, signs that Canada’s largest trading partner, the U.S., may be facing a slowing economy is ultimately bad for the Canadian dollar, as is the underperformance in energy markets. (Energy accounts for 11% of Canadian GDP).

Strategy (23DTE, ATM) | Strikes | POP | Max Profit | Max Loss |

Iron Condor | Long 0.7175 p Short 0.72 p Short 0.745 c Long 0.7475 c | 77% | +50 | -200 |

Long Strangle | Long 0.7175 p Long 0.7475 c | 15% | x | -80 |

Short Put Vertical | Long 0.7175 p Short 0.72 p | 91% | +30 | -220 |

Christopher Vecchio, CFA, tastylive’s head of futures and forex, has been trading for nearly 20 years. He has consulted with multinational firms on FX hedging and lectured at Duke Law School on FX derivatives. Vecchio searches for high-convexity opportunities at the crossroads of macroeconomics and global politics. He hosts Futures Power Hour Monday-Friday and Let Me Explain on Tuesdays, and co-hosts Overtime, Monday-Thursday. @cvecchiofx

Thomas Westwater, a tastylive financial writer and analyst, has eight years of markets and trading experience. @fxwestwater

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.