What Do Bond Yields Say About the Economy?

What Do Bond Yields Say About the Economy?

Trader Econ 101: How to read a yield curve

- Yield curves can gives us insight into how the bond market views economic risks and potential changes in monetary policy.

- There are three different yield curve shapes: normal, flat and inverted.

- Contrary to popular opinion, the 2s10s spread is not the most important yield curve spread to watch to predict recessions.

Reading the yield curve

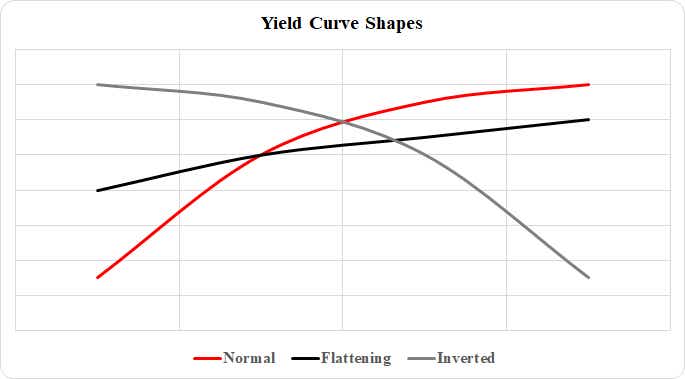

The yield curve shows how the yields of bonds with different maturities vary depending on the level of risk and the time horizon. A “normal” yield curve is upward sloping, meaning bonds with longer maturities have higher yields than bonds with shorter maturities. This is because investors demand more compensation for lending money for longer periods because there is more uncertainty and risk involved. A positive sloping yield curve reflects this “normal” relationship.

By looking at a government bond yield curve (such as U.S. Treasuries), one can make some judgments about the economic situation at any given time. For example, if the short-term rates are rising fast, this could indicate the central bank is planning to raise interest rates soon. Or it could mean the government is facing some funding problems.

On the other hand, if the long-term rates are falling sharply, this could suggest the prospects for economic growth are weakening. Or it could mean the government’s creditworthiness is improving. The context matters a lot.

What’s a flattening yield curve?

A flattening yield curve means the difference between the yields of long- and short-term bonds is narrowing. This happens when the yields of short-term bonds increase or the yields of long-term bonds decrease, or both.

For example, if a bond with a two-year maturity has a yield of 2%, and a bond with a 10-year maturity has a yield of 4%, the difference is 200 basis points. If the two-year yield goes up to 2.5%, and the 10-year yield goes down to 3.5%, the difference is now 100 basis points. The curve becomes flatter.

A flattening yield curve can signal the economy is slowing down and that inflation and interest rates are expected to remain low for a long time.

What is a steepening yield curve?

A steepening yield curve means the difference between the yields of long- and short-term bonds is widening. This happens when the yields of long-term bonds increase more than the yields of short-term bonds, or when the yields of short-term bonds decrease while the yields of long-term bonds increase.

For example, if a bond with a two-year maturity has a yield of 2%, and a bond with a 10-year maturity has a yield of 4%, the difference is 200 basis points. If the two-year yield goes up to 2.25%, and the 10-year yield goes up to 4.5%, the difference is 225 basis points. The curve becomes positively steeper.

A steepening yield curve can indicate the economy is growing stronger and that inflation and interest rates are expected to rise in the future.

What is an inverted yield curve?

Sometimes, the yield curve can become inverted, which means the yields of short-term bonds are higher than the yields of long-term bonds. This happens when investors expect interest rates to fall in the future, so they demand higher returns for holding short-term bonds than long-term bonds.

For example, if a bond with a two-year maturity has a yield of 2%, and a bond with a 10-year maturity has a yield of 4%, the difference is 200 basis points. If the two-year yield goes up to 2.5% and the 10-year yield goes down to 2%, the difference is now -50 basis points. The curve becomes negatively steeper or inverted.

An inverted yield curve can signal investors are pessimistic about the future of the economy and expect deflation and lower interest rates.

Which curve matters the most?

Duke University finance professor Campbell Harvey explored the idea of using the yield curve to forecast recessions in his 1986 dissertation. Contrary to popular opinion, the 2s10s spread (10-year yield minus two-year yield) is not the yield curve to watch.

Professor Harvey’s research indicates the 3m10s (10-year yield minus three-month yield) is the key yield curve, and it needs to invert for at least one full quarter (or three months) to give a true predictive signal (since the 1960s, a full quarter of inversion has predicted every recession correctly). The New York Federal Reserve tracks the 3ms10s spread to calculate the probability of a recession over the next 12-months.

Christopher Vecchio, CFA, tastylive’s head of futures and forex, has been trading for nearly 20 years. He has consulted with multinational firms on FX hedging and lectured at Duke Law School on FX derivatives. Vecchio searches for high-convexity opportunities at the crossroads of macroeconomics and global politics. He hosts Futures Power Hour Monday-Friday and Let Me Explain on Tuesdays, and co-hosts Overtime, Monday-Thursday. @cvecchiofx

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.