What Causes Volatility to Expand?

What Causes Volatility to Expand?

Two events often lead to significant increases in volatility: market drops & binary events

- Much like the market itself, volatility expansions or contractions are largely random and unpredictable.

- Volatility expansions can, however, be directly tied to binary events in the market, such as FOMC or earnings.

- Volatility contractions are sort of the default state of the market as it slowly rises over time.

A quick dive into any options pricing model shows more volatility leads to more extrinsic value, and less volatility leads to less extrinsic value. And if we’re focused on purely out-of-the-money options, we’re only dealing with extrinsic value in the option price because intrinsic value exists only for in-the-money options. So, what causes volatility to expand or contract, which in turn directly affects option pricing by way of increasing or decreasing extrinsic values?

Well, volatility itself is a random entity in the market, just like everything else. Stock prices are random and unpredictable. Market variables are random and unpredictable. Therefore, market volatility is random and unpredictable. But if we focus on expansion, two events often lead to significant increases in volatility: market drops and binary events.

Volatility expansion

Market volatility and market prices are inversely related most of the time, so if the market suddenly drops a sizeable amount, there is a good chance volatility will expand rapidly. This relationship can be established mathematically, but one way to intuitively understand this is that the market usually rises over time, so a large drop can obviously spook a lot of investors, leaving them feeling a lot more uncertain about the future. As a result, market volatility rises to reflect that added uncertainty felt by investors.

Regarding binary events, such as a Federal Reserve announcement or company earnings report, the possibility of large moves because of these events is higher than it would be for a normal day. Therefore, to reflect this increased possibility of a big move, volatility will often rise leading into these events.

Volatility contraction

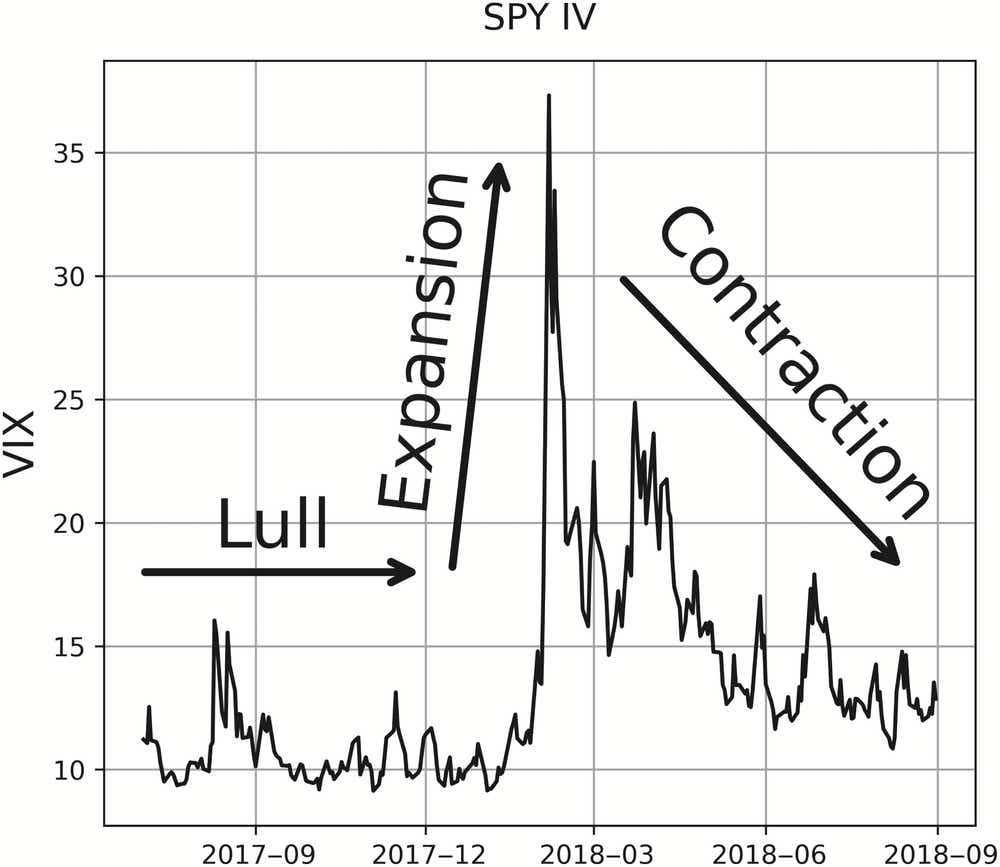

Market volatility needs a catalyst to remain elevated. Otherwise, it will collapse under its own weight and fall back down to earth. Therefore, on the contraction side, given the inverse relationship between market price and market volatility that we just mentioned, and a market that wants to grind higher over time, you end up with market volatility usually in a state of contraction. In fact, according to Figure 2.2 inside The Unlucky Investor’s Guide to Options Trading (below), the market is either in a “lull” state, in which volatility is slowly dropping, or a “contraction” state, where volatility quickly crashes, approximately 90% of the time.

Jim Schultz, a quantitative expert and finance Ph.D., has been trading the markets for nearly two decades. He hosts From Theory to Practice, Monday-Friday on tastylive, where he explains theoretical trading concepts and provides a practical application of those concepts to a trading portfolio. @jschultzf3

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.