U.S. PCE Inflation Data: Jittery Markets Fear Fed Rate Cut Delay

U.S. PCE Inflation Data: Jittery Markets Fear Fed Rate Cut Delay

By:Ilya Spivak

The markets are angling for Fed rate cuts as growth slows after a blockbuster third-quarter U.S. GDP surge. Panic might follow if PCE inflation data hints at a delay.

- Financial markets are in a worried mood after blockbuster third-quarter U.S. GDP data.

- Price action across key assets signals traders are envisioning a peak in the business cycle.

- U.S. PCE inflation data may spark a knee-jerk volatility if Fed rate cuts look less certain.

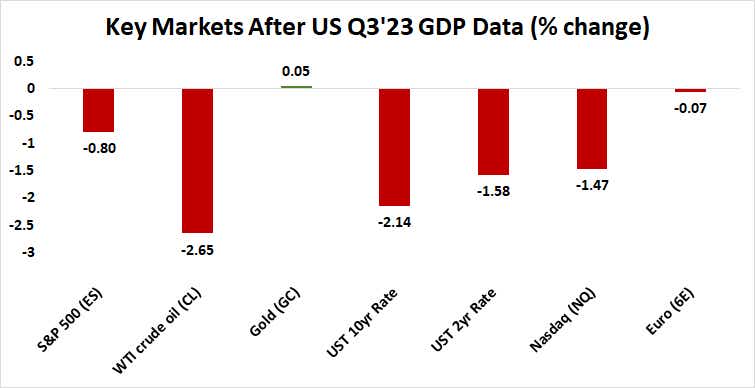

The markets offered a circumspect response as U.S gross domestic product (GDP) data showed economic growth surged in the third quarter.

Output grew at a blistering annualized rate of 4.9%, sailing past forecasts expecting to see 4.5%. That’s the fastest performance since the fourth quarter of 2021, when a surge of catch-up growth after the worst of the COVID-19 pandemic crested at 7%.

After a bit of jostling to digest the outcome, the markets settled on a verdict: risk off.

Wall Street lurched down across the major indices, with the Nasdaq leading the down trend as the heavy-lifting tech sector suffered outsized losses. What little green there was to see showed up in defensively minded real estate, materials, and utilities names. Consumer-linked shares and energy saw significant selling.

Meanwhile, bonds rallied across the maturity spectrum, pushing the yield curve broadly lower. Gold prices continued to inch higher but crude oil prices fell, seemingly separating today’s price action from their parallel response to escalating geopolitical strife in the Middle East. The U.S. dollar idled against its major counterparts.

Financial markets see economic pain ahead

Taken together, this seems to say that the markets saw the GDP report as marking a peak in growth rather than setting the stage to build on strength. A Bloomberg survey of economists has economic growth slowing to a meager 0.8% in the fourth quarter and staying below 1% until the second half of 2024.

The response across the asset spectrum appears to look ahead to leaner economic times, where sensitivity to the business cycle is a mark of weakness and the Federal Reserve can set the stage for interest rate cuts.

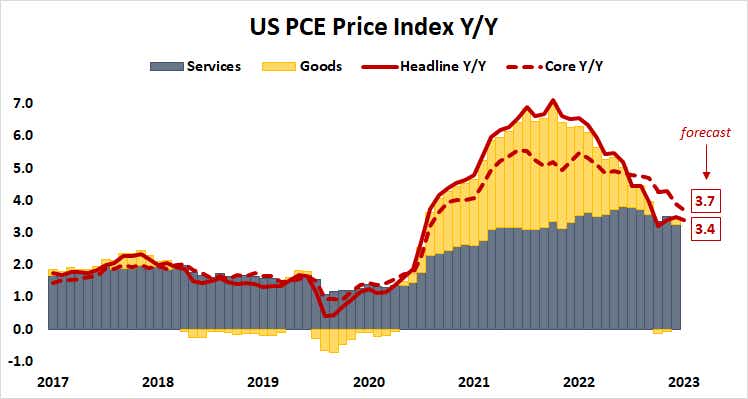

A sense of panic might take hold if confidence in the Fed’s part of that story wavers. With that in mind, the spotlight now turns to September’s personal consumption expenditure (PCE) inflation gauge, the U.S. central bank’s favored yardstick. It is expected to show orderly disinflation continuing, with the core rate down to 3.7% from 3.9% previously.

U.S. inflation data: reasons to worry?

That seems to set the stage for an uneventful release, yet such assumptions are difficult to make as jittery markets jump from one headline to the next.

Traders’ response to analog consumer price index (CPI) data earlier this month is a case in point. They seized on a narrowly higher-than-expected headline inflation reading even as the more Fed-relevant core price growth measure fell. “Higher-for-longer” fears resurfaced, bond yields swung higher, and stocks swooned.

The message that financial markets have for U.S. central bank officials seems clear: “We want rate cuts.” As it stands, the first 25-basis-point reduction is expected no later than July 2024. The markets are nearly certain that three cuts are on the menu by year-end, assigning that outcome a 97% probability.

Anything that appears to delay the easing cycle or reduce its scope is likely to be taken poorly.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.