Global PMI Data: Markets Face the Dark Side of U.S. Economic Strength

Global PMI Data: Markets Face the Dark Side of U.S. Economic Strength

By:Ilya Spivak

Disparate global growth is a potent risk for the markets.

- January PMI data to show the U.S. continues to boom as Europe struggles

- U.S. exceptionalism is exporting higher interest rates, and not much else

- Markets may shudder if global growth trends become even more lopsided

The U.S. economy remained the envy of the world in January, according to analysts’ expectations for purchasing managers index (PMI) data due from S&P Global this week. The composite gauge tracking economic activity growth in manufacturing and the service sector is expected to hold near December’s reading, which was the highest since April 2022.

By contrast, results from the Eurozone are likely to remain anemic. Median forecasts envision the third consecutive month of contraction as lackluster growth on the services side struggles to offset a deep manufacturing slump. January would thus mark the worst three months in a year for the currency bloc’s economy.

PMI data to show the U.S. still stands alone on economic growth

This paints a troubling picture for global growth at large. Together with China, the U.S. and the Eurozone account for 58% of worldwide gross domestic product (GDP). The remaining 42% are largely made up of vendor economies that depend on demand from the “big three” to power growth of their own.

China has struggled to grow after emerging from “zero Covid” lockdowns in late 2022 despite waves of stimulus. The markets hope to see a more concerted fiscal effort at revival to appear at the National People’s Congress (NPC) in March, but Beijing has disappointed such mythmaking before.

Meanwhile, the boom in the U.S. is mostly aiming inward. Last week, U.S. consumer price index (CPI) data showed that the service sector accounted for close to 93% of overall price growth. Such lofty readings have been the norm since 2023. By contrast, the averages for 2021 and 2022 are 36% and 42% respectively.

Markets may shudder if global growth disconnect gets worse

Most U.S. services demand is satisfied domestically, whereas most imports are on the goods side of the ledger. This helps explain how the global economy seems to be struggling to build escape velocity even as its largest contributor soars into the stratosphere. The sorry state of Canada’s economy – which mostly exports to the U.S. – is a case in point.

What’s more, there is a dark side to U.S. outperformance: rising interest rates. Borrowing costs have surged globally as traders have repriced for fewer Federal Reserve rate cuts in 2025 over recent months. The ubiquity of the dollar in global commerce means that in managing domestic lending rates, the Fed steers the worldwide cost of money too.

This comes at a most inconvenient time, as 2025 brings large scale bond and loan redemptions across the global economy. Refinancing at significantly higher rates will become more onerous if U.S. strength continues to drive up yields. Lopsided worldwide growth will make that difficult to stomach.

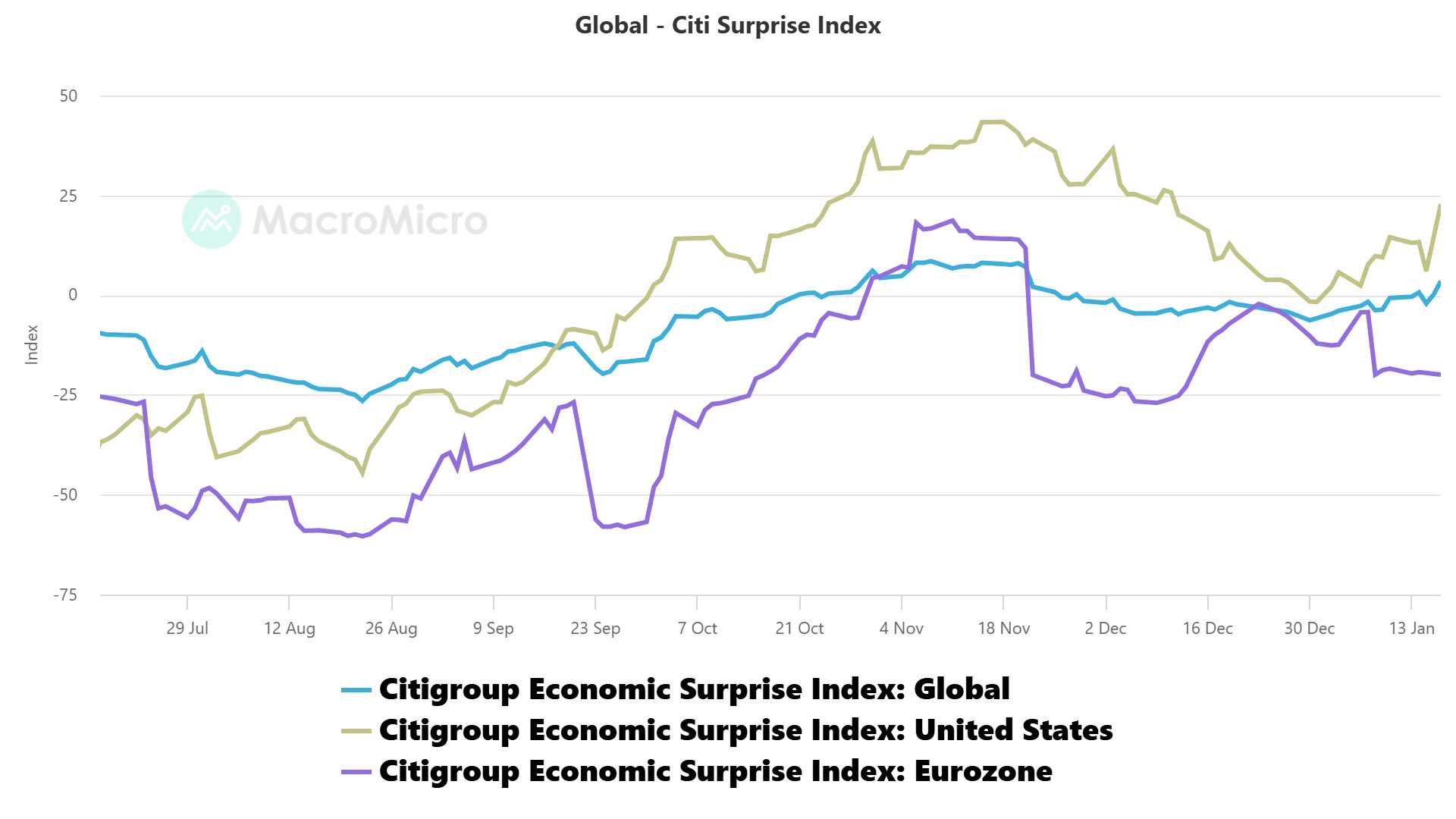

A wider U.S.-favoring disparity on offer in the PMI data may thus begin to spook the markets worried about liquidity risk and credit market stress. Analytics from Citigroup warn of just such a scenario. They show U.S. economic news flow increasingly outperforming baseline forecasts, while the trend for the Eurozone points in the opposite direction.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.