U.S. Jobs Data, Fed Powell Speech, Eurozone CPI, RBA Meeting: Macro Week Ahead

U.S. Jobs Data, Fed Powell Speech, Eurozone CPI, RBA Meeting: Macro Week Ahead

By:Ilya Spivak

A flood of macro event risk threatens to overwhelm jittery financial markets

- Traders look to RBA commentary to gauge emerging risks to global growth.

- Cooling Eurozone inflation unlikely to burden the euro amid defense buildout.

- U.S. ISM and employment data, Fed Chair Powell speech take center stage.

Stock markets succumbed to selling pressure last week, roiled by renewed worries about incoming U.S. tariffs and their disruptive potential for economic growth. President Donald Trump has talked up August 2 as the date “reciprocal” trade barriers would go into effect, amounting to a sharp and broad-based rise in import costs.

The bellwether S&P 500 fell 1.7% while the tech-oriented Nasdaq 100 shed 2.5%. Treasury yields fell sharply at the end of the week after struggling to balance anti-risk demand with interest rate cut speculation, to seemingly resolve the impasse in favor of dovish mythmaking. Gold prices tellingly surged to a record high. The U.S. dollar weakened modestly.

Against this backdrop, here are the key macro waypoints to consider in the days ahead.

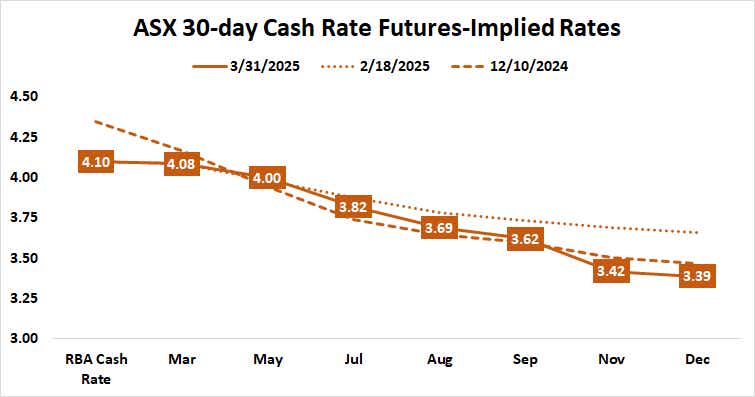

Reserve Bank of Australia (RBA) monetary policy meeting

Australia’s central bank is expected to keep its target interest rate unchanged at 4.1% after this week’s policy meeting. Interest rate futures show markets have priced in 69 basis points (bps) in cuts this year, implying two standard-sized 25bps reductions and a 76% probability of a third one.

Inflation eased to a four-year low of 2.4% year-on-year in the fourth quarter but purchasing managers index (PMI) data suggests a rebound in domestic demand fueled the fastest pace of economic growth in seven months in March. Traders will be keen to hear how the RBA expects to balance these influences alongside an uncertain global backdrop.

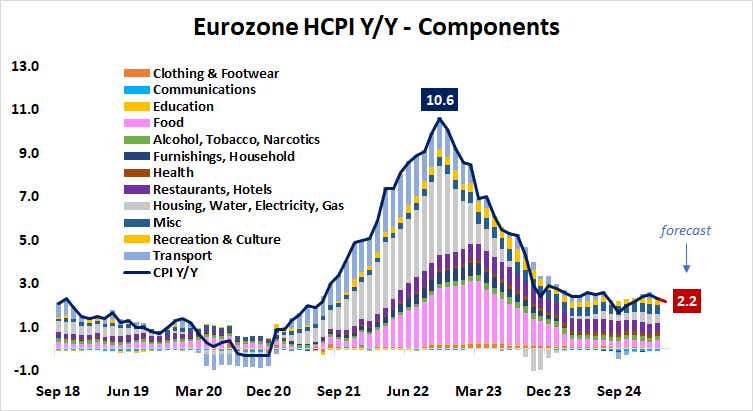

Eurozone consumer price index (CPI) data

Inflation is expected to have slowed to in the Euro Area in March. The headline price growth rate is expected to inch down to 2.2% year-on-year, the lowest since November. That may do little to inspire a dovish rethink of European Central Bank (ECB) rate cut bets however, as markets look ahead to an incoming wave of defense spending.

As it stands, the markets price in 65bps in rate cuts this year. The bias flips toward rate hikes in 2026, with traders discounting a 40% probability of a 25bps increase. Analytics from Citigroup hint that Eurozone data has tended to outperform forecasts recently, opening the door for an upside surprise that might amplify hawkish speculation.

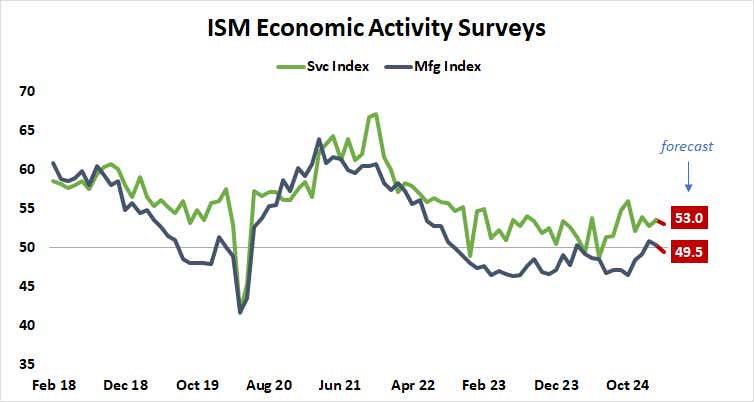

ISM purchasing managers index (PMI) data

PMI surveys from the Institute of Supply Management (ISM) will help shape expectations for U.S. economic growth as recession fears remain front-of-mind for financial markets. Economists expect manufacturing to regress into contraction mode for the first time since December while the pace of service sector growth cools from a two-month high.

Traders comb through the data for evidence about the impact of fiscal policy uncertainty, especially on tariffs. That has been a running theme in analog S&P Global PMI figures that have rattled the markets since late February. Signs pointing to cooling confidence on the services side – the dominant driver of overall growth – may be most concerning.

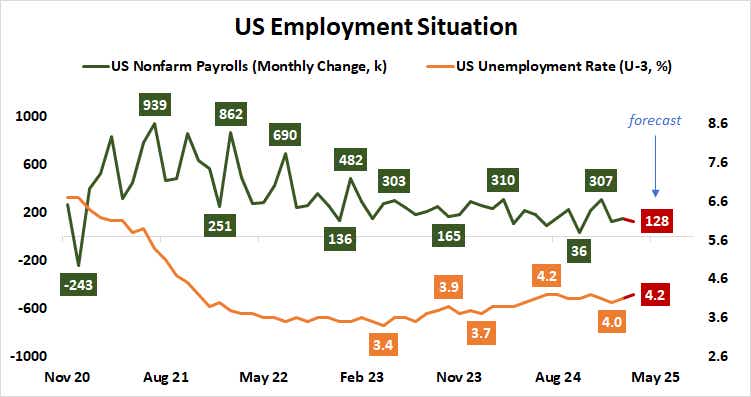

U.S. employment data & Fed Chair Powell speech

Job creation is expected to have slowed in the U.S. in March. Baseline forecasts point to a rise of 128,000 in nonfarm payrolls. That would mark a cooldown from the 151,000 added in the prior month. It would also make the third quarter the slowest three-month period for job creation since mid-2020, when COVID-19 lockdowns led to mass layoffs.

A mere three hours after the figures cross the wires, Federal Reserve Chair Jerome Powell will take to the microphone for a speech updating markets on the outlook for the U.S. economy. Speaking at the press conference after the March policy meeting, Powell said that the Fed is waiting for “hard data” to validate emerging signs of economic stress.

If the ISM and jobs reports suggest that its time for the U.S. central bank to step up its efforts, the markets are likely to be disappointed with another “wait-and-see” directive from the Fed Chair. That may lead stock markets, Treasury yields, and the U.S. dollar lower in tandem.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.