Fed Chair Powell Testimony, U.S. CPI Inflation and Retail Sales Data: Macro Week Ahead

Fed Chair Powell Testimony, U.S. CPI Inflation and Retail Sales Data: Macro Week Ahead

By:Ilya Spivak

Stock markets struggle for direction, but long-end Treasury rates are dropping. Powell is likely to repeat a “gradualist” mantra.

- Stock markets are struggling for direction, but long-end Treasury rates are dropping.

- Fed Chair Powell will likely repeat a familiar “gradualist” mantra in testimony.

- U.S. CPI inflation and retail sales data may leave concern about growth intact.

Wall Street struggled to shrug off another rough start of trading last week, this time thanks to confusion about U.S. tariffs on imports from Canada and Mexico. The bellwether S&P 500 index fell 0.3%, marking a second consecutive decline. The tech-tilted Nasdaq 100 fared only a bit better, finishing flat after losing 1.5% in the previous week.

However, most of the action was in the bond market. Steady Federal Reserve policy bets made for stability at the front end of the yield curve, but longer-dated rates continued to fall. In fact, the benchmark 10-year Treasury yield reached the lowest point in eight weeks. That came in the wake of surprisingly weak U.S. service-sector data.

Against this backdrop, here are the key macro waypoints to consider in the days ahead.

Federal Reserve Chair Jerome Powell testimony

The time has come for Fed Chair Powell to head up to Capitol Hill and sit for the obligatory two days of semi-annual testimony updating legislators on monetary policy. The central bank chief will appear in the Senate first, then go in for a repeat performance at the House of Representatives.

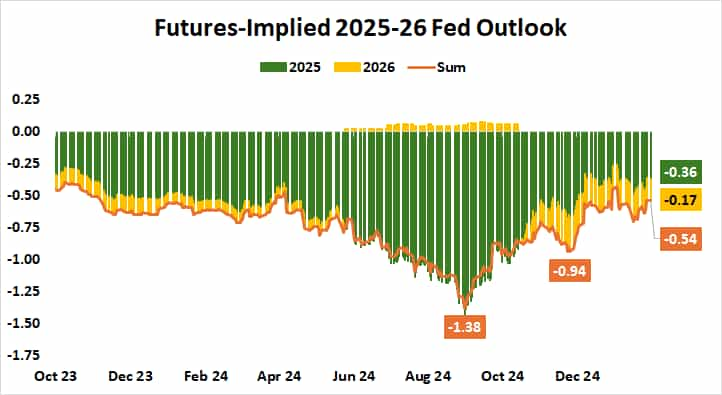

As it stands, the markets are priced for a more hawkish rates path than Fed officials have projected. Fed funds futures have discounted 54 basis points in cuts through the end of next year, amounting to half of what the rate-setting Federal Open Market Committee (FOMC) penciled into its forecasts in December.

For his part, Powell will probably repeat a familiar gradualist mantra, arguing that the Fed remains in fine-tuning mode and feels no need to adjust in a hurry. This might endorse the sense that delay now may translate into deeper cuts downwind, as the recent drop at the long end of the yield curve seems to anticipate.

U.S. consumer price index (CPI) data

U.S. inflation is expected to have made some modest progress lower in January. While the headline reading is seen holding unchanged at 2.9% year-on-year for a second consecutive month, the core measure excluding volatile food and energy prices is projected to inch lower to 3.1%. That would be the slowest since April 2021.

Leading purchasing managers index (PMI) data endorses the likelihood that cost pressures eased a bit last month. Moreover, analytics from Citigroup suggest U.S. economic data outcomes have anchored close to baseline forecasts since the beginning of the year, implying that surprise risk is relatively low.

.png?format=pjpg&auto=webp&quality=50&width=758&disable=upscale)

U.S. retail sales data

Economists’ median forecasts suggest retail sales activity cooled a bit last month. A -0.1% downtick from the prior month is expected, marking the first negative reading since June. Household consumption is by far the largest contributor to overall economic growth, and traders will be keen to see if something more sinister is brewing.

That’s after a shocking disappointment on a closely watched gauge of U.S. consumer confidence from the University of Michigan (UofM). It showed sentiment has fallen to a three-month low as one-year inflation expectations surged to 4.3%, the highest since November 2023. Survey respondents cited the risk of rising tariffs as an outsized concern.

.png?format=pjpg&auto=webp&quality=50&width=735&disable=upscale)

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.