Russia, Ukraine and Global Wheat Prices

Russia, Ukraine and Global Wheat Prices

By:Ilya Spivak

No panic yet for the wheat market as Russia moves to cut Ukraine out

- Russia delivers on threats by suspending Black Sea grain deal.

- Wheat prices are staying in downtrend despite Ukraine shut-out.

- Moscow’s market-share push is keeping key exports cheap.

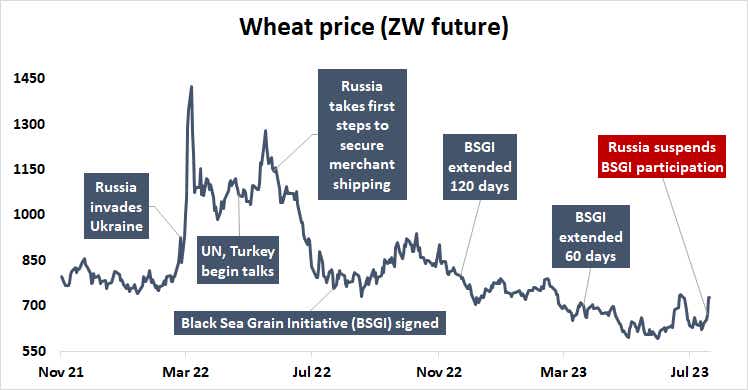

Wheat prices seemed somewhat unimpressed as Russia finally made good on months of on-and-off saber-rattling and suspended its participation in the Black Sea Grain Initiative (BSGI). This is a United Nations- and Turkey-sponsored scheme meant to allow safe passage for Ukrainian grain exports to global markets in wartime without Russian molestation.

Wartime grain deal ends with a whimper

A bit of a panicky pop was certainly registered: the benchmark ZW wheat futures contract jumped 8.5% on the day the Kremlin’s decision went into effect. That sounds like a very large rise at first. In fact, it only marginally exceeds the recent baseline range of +/- 6% to 7% swings prevailing since March 2022, when the initial shock of Russia’s invasion of Ukraine began to settle. The 11% to 22% daily seesaw clocked in the first few weeks of the conflict was far more dramatic.

Perhaps most importantly, the move fell short of clearing the most recent swing high in late June and kept the structural downtrend in play for the past 14 months firmly intact. In 2021—the last full pre-war year—Ukraine was the world’s fifth largest wheat exporter, accounting for 9.5% of global shipments. That is no trivial contribution, so it seems natural to wonder why a stronger reaction was not had.

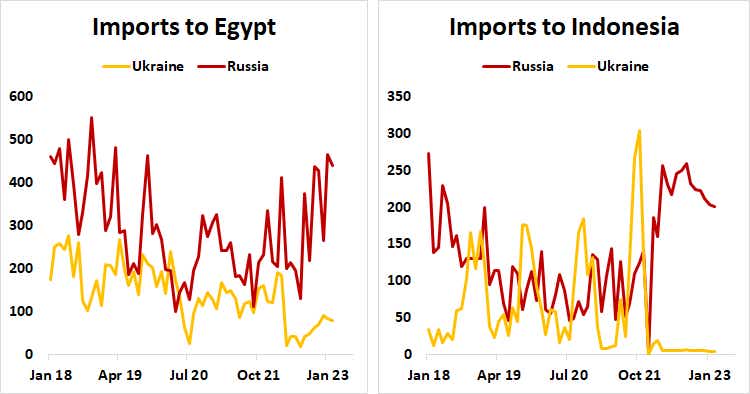

Ukrainian wheat exports hobbled by conflict, BSGI or not

A look at how trade flows from Russia and Ukraine to the world’s top wheat importers have evolved over the course of the conflict make the answer obvious as well as tragic: Ukrainian contribution to the global wheat trade has been hobbled to such an extent—with BSGI active or without it—that the scheme’s end seems unlikely to make a material dent in global supply.

As much can be readily seen from overall import volumes to Egypt and Indonesia, the world’s largest and third-largest wheat buyers, where Russia and Ukraine were reasonably competitive with each other before the conflict. Markets like China, Turkey and Nigeria rounding out the top five global importers have maintained a strong preference for Russian product for years before the war’s beginning.

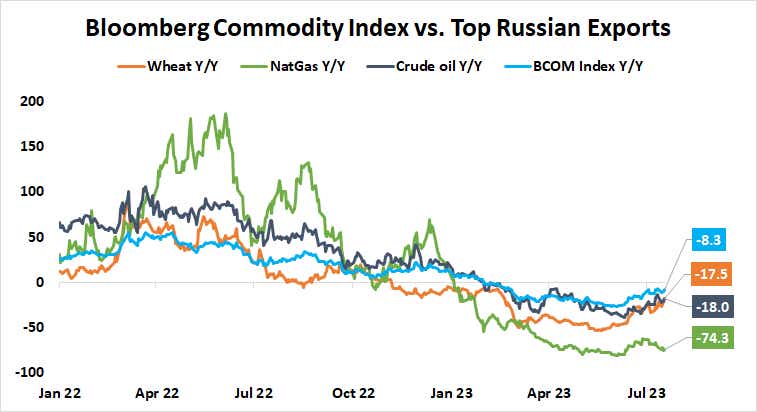

Top exports on discount as Russia fights for market share

Meanwhile, trying to keep commodities cheap on global markets when Russia is a dominant exporter seems to be a part of the Kremlin’s military strategy. Prices for the top three—wheat, crude oil and natural gas—are down significantly more year-on-year than the Bloomberg average of global raw materials costs.

Moscow is probably trying to protect its market share even as it is hamstrung by Western sanctions. It has but a few outlets left to raise money, including for the war. Giving up ground would be doubly damaging since the main competition in key markets is from countries backing Ukraine in the conflict, most notably the United States. It commands a 12.7% slice of the market, second only to Russia itself.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.