U.S. PCE Preview: Will Lower Inflation Revive the Ailing Stock Market?

.png?format=pjpg&quality=50&width=1760&disable=upscale&auto=webp)

U.S. PCE Preview: Will Lower Inflation Revive the Ailing Stock Market?

By:Ilya Spivak

Stock markets may continue to sink despite cooling U.S. PCE inflation data.

- Global recession fears hit financial markets amid signs of U.S. slowdown

- Fed rate cut expectations turn increasingly dovish as traders get defensive

- U.S. PCE inflation data is unlikely to turn the risk-off drive on Wall Street

Worries about a slowdown of U.S. growth have gripped financial markets as deteriorating data flow warns that last year’s explosive outperformance in the world’s largest economy is unraveling. Signs of trouble have trickled in since the beginning of the year, but February’s S&P Global purchasing managers index (PMI) data was most sobering.

The report showed that economic activity growth has nearly stalled. The pace of expansion slowed sharply to the weakest in 17 months. Most ominously, the weakness came from the mission-critical service sector, which recorded its first contraction in 25 months. New orders growth fizzled, and business sentiment soured.

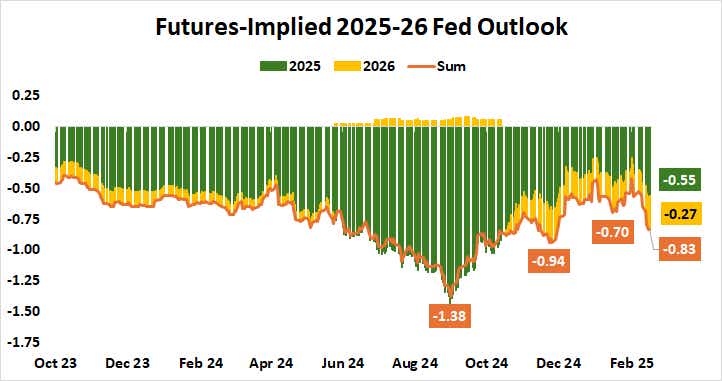

Recession fears are stoking Fed interest rate cut speculation

In turn, this means that global recession risk is building. Throughout the second half of 2024, the U.S. stood alone as a pillar of economic strength while the other major drivers of worldwide growth – the Eurozone and China – slumped toward standstill. They remain there still, even as the U.S. appears to converge on their malaise.

Not surprisingly, this has translated into dovish repricing of Federal Reserve monetary policy expectations. Just one week ago, benchmark Fed Funds interest rate futures were pricing in 55 basis points (bps) in cuts through the end of 2026. That tally has now grown to 83bps. Moreover, rates are down across the yield curve, the front and the long end.

With this in mind, the spotlight turns to the personal consumption expenditure (PCE) measure of U.S. inflation, the Fed’s favored barometer for price growth. The headline reading is expected to bring a shallow downtick to 2.5% year-on-year in January, marking a modest improvement from the 2.6% recorded in the prior month.

Stocks may fall further after U.S. PCE inflation data

The core PCE measure excluding volatile food and energy prices is expected to come down to 2.6% year-on-year, the lowest since June 2024. That may seem encouraging for traders hoping the Fed will move faster to step in with stimulus, but markets have almost certainly priced in baseline expectations already at this point.

.png?format=pjpg&auto=webp&quality=50&width=754&disable=upscale)

Furthermore, the PCE report is generally unlikely to offer up big deviations from the analyst consensus. That’s because it comes after consumer (CPI) and producer (PPI) price measures in the data reporting cycle. Those outcomes inform PCE prognostications, making for relatively accurate forecasting.

On balance, this means the incoming report may be more notable for its passing than its substance. Results that hew closely to median expectations may leave the markets without much of a new lead, setting the stage for a return to the latest default. For stock markets, that has pointed firmly lower this week.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.