Key U.S. And Chinese Trade and Inflation Data May Flag Recession Risk

Key U.S. And Chinese Trade and Inflation Data May Flag Recession Risk

By:Ilya Spivak

Macro events that may move the markets this week

- Stocks and the dollar see reversals after U.S. jobs data warns of bubbling recession fears.

- Chinese trade and inflation reports may disappoint, stoking growth concerns.

- Markets may downgrade Fed rate cut odds if U.S. CPI data tops expectations.

The markets offered a curious response after July’s U.S. employment report crossed the wires on Friday, Aug. 4.

The headline increase in non-farm payrolls fell slightly short at 187,000 against expectations of 200,000. The jobless rate surprised at a slightly lower-than-projected 3.5%. Average hourly earnings numbers showed wage inflation was a bit faster than anticipated at 4.4% year-over-year. In all, none of the key readings veered too far from forecasts.

Initially, Treasury yields fell alongside the U.S. dollar, as the odds for another Fed rate hike in 2023 declined after the release while stocks idled. Then, a wave of selling hit Wall Street just ahead of the weekly close. Stocks tumbled while the Greenback rose, even as rates held near daily lows. The anti-yield Japanese yen was tellingly higher, too.

This sudden splash of telltale “risk off” price action ahead of the weekend might speak to increasing worries about recession. The Fed estimates it can take 12 to 18 months for the impact of a single rate rise to be fully absorbed into the economy. So, pressure from the bulk of last year’s outsized 50- and 75-basis-point rate hikes ought to be appearing right about now.

Economic data on tap this week will test the markets’ sensitivity to growth concerns and might reveal recalibration in the way traders interpret economic data outcomes.

Chinese trade and inflation data

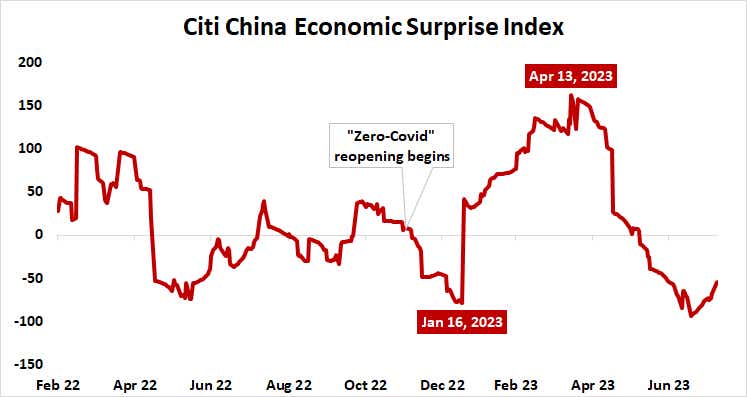

China is expected to report that the economic recovery after reopening from “zero-COVID” restrictions in December 2022 continues to struggle. July trade data due on Tuesday is seen showing steep losses in both exports and imports once again. Forecasts call for declines of 12.4% and 6.8% year-over-year, respectively. Inflation data due on Wednesday is expected to remain anemic, with the consumer price index down 0.4% year-over-year after idling in June.

Chinese economic data has increasingly underperformed relative to expectations in recent months, according to data out of Citigroup. That sets the stage for downside surprises that might amplify global recession fears, which may broadly weigh on stocks and rates while boosting bonds, the U.S. dollar and the Japanese yen once again.

U.S. consumer price index

Thursday brings July’s U.S. consumer price index (CPI) data. The headline rate is expected to rise to 3.3% year-over-year, up from 3.0% in June. Unlike China, U.S. economic data has tended to outperform relative to expectations since mid-May, the latest jobs report notwithstanding. If that inspires markets to reprice bets on the start of a rate hike cycle by the second quarter of 2024, worries about the negative growth implications of a “higher-for-longer” Fed policy path might trigger still more “risk off” price action across benchmark asset classes.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.