U.S. CPI Preview: Will Still More Inflation Sink the Stock Market?

U.S. CPI Preview: Will Still More Inflation Sink the Stock Market?

By:Ilya Spivak

Will the markets lose faith in Fed interest rate cuts altogether?

- Wall Street struggles to make good on modestly helpful U.S. PPI report

- All eyes now turn to U.S. CPI data, with Fed rate cut speculation in focus

- “Buy the rumor, sell the fact” dynamics may be in play for Treasury yields

Wall Street struggled to make hay of U.S. producer price index (PPI) that showed slower wholesale inflation than economists anticipated. Factory-gate prices grew 3.3% year-on-year in December, a touch lower than median forecasts calling for 3.4%. Nevertheless, the print marked an uptick to the highest reading since February 2023.

The core PPI measure excluding volatile food and energy prices came in 3.5% year-on-year, undershooting expectations of a rise to 3.8%. That matched the revised reading for November, which was adjusted a bit higher from the originally reported 3.4%. As with the headline figure, these outcomes amounted to 22-month highs.

Stock markets resist the urge to bounce on helpful U.S. PPI data

The bellwether S&P 500 popped briefly higher alongside Treasury bonds as yields spiked down when the PPI data set came across the wires. The impact scattered within a mere 15 minutes however, leaving stocks and interest rates trading close to flat. Gold prices rose as the U.S. dollar cooled, but those moves began before the PPI release.

.png?format=pjpg&auto=webp&quality=50&width=758&disable=upscale)

Markets have shown themselves to be highly reactive to news flow that shapes the expected trajectory Federal Reserve monetary policy and with it the baseline cost of borrowing. However, PPI was seemingly insufficient to inspire directional commitment as traders await the higher-profile consumer price index (CPI) report.

Headline CPI is expected to have accelerated for a third consecutive month in December, rising to 2.9% year-on-year. That would mark the highest reading since July. The core reading—a focal point for the Fed since it has little agency over global food and energy costs—is seen holding at 3.3% year-on-year for the fourth month straight.

U.S. CPI inflation: buy the rumor, sell the fact?

CPI figures have run a bit faster than the closely watched “nowcast” topline projection from the Cleveland Fed for the past three months. Moreover, Citigroup analytics point to accelerating outperformance on overall U.S. economic data outcomes relative to baseline forecasts are once again.

That may set the stage for an upside surprise, an outcome that might be expected to drive yields higher and weigh on stock markets. However, scope for any such move will have to contend with how much hawkish repositioning has already transpired.

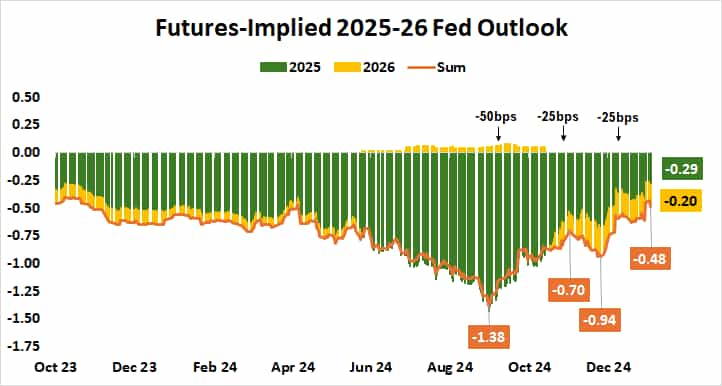

As it stands, benchmark Fed Funds futures have priced in just 29 basis points (bps) in cuts this year. This implies that traders have discounted just one standard-sized 25bps rate cut and a meager 16% probability of a second one. For its part, the U.S. central bank officials’ median view call for 50bps in stimulus.

Pushing expectations to a still more hawkish setting from here would amount to accepting that the Fed may forgo cuts altogether. That may be a bridge too far given Fed officials’ loud insistence on some easing this year, at least for now. With that in mind, anything but a shockingly high CPI reading may counterintuitively cap Treasury yields.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.