Can a Rate Hike Breathe Life into the Euro?

Can a Rate Hike Breathe Life into the Euro?

By:Ilya Spivak

The euro looks deeply troubled as prices flatline even amid growing expectations of another ECB interest rate hike

- Reuters reports the ECB will lift its inflation outlook while cutting economic growth projections.

- Markets respond with a hawkish shift in ECB rate hike bets, but the euro looks the other way.

- Sellers may drive the currency lower if the central bank opts to move into wait-and-see mode.

The euro is struggling even as markets move to price in an interest rate hike from the European Central Bank (ECB) this week. That bodes ill for the single currency.

At the start of this week—a mere 48 hours ago—swaps market pricing reflected a cumulative 75% probability that the ECB will issue another 25-basis-point rate hike before the end 2023. September was seen as the meeting when the increase was most likely—with a probability of 41%.

This calculus has changed. Reuters reported that the central bank will upgrade its inflation outlook to put price growth above 3% next year while downgrading the economic growth outlook for this year and 2024, citing an anonymous source “with direct knowledge of the matter."

That activated a hawkish rethink in the markets. One more rate hike for this year is now fully priced. September is still seen as the likeliest time for the increase, with a probability of nearly 65%. It is expected to be reversed by mid-year with the start of an easing cycle.

Currency markets yawned at the adjustment. The euro is trading little-changed against a basket of its major counterparts. It is on course to finish the day flat against the U.S. dollar. That speaks to potent underlying weakness. Any asset unable to find strength in such a textbook example of supportive news-flow seems to be deeply unloved by investors.

Markets unimpressed even as ECB rate hike expectations grow

The markets’ skepticism echoes the deep predicament facing ECB officials, and the way in which they seem likeliest to address it.

The latest round of purchasing managers index (PMI) data neatly summarizes a steady stream of downbeat Eurozone economic data, showing the regional economy shrank for a second month in August. Meanwhile, inflation expectations priced into the bond and swaps markets are trending stubbornly higher. This adds up to divergent policy cues.

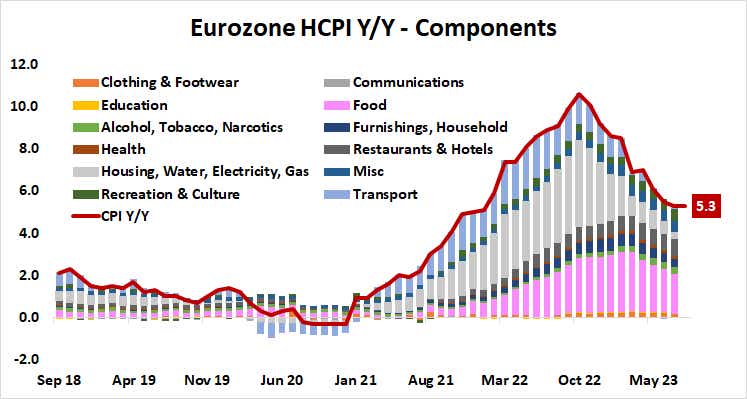

At this point, Eurozone inflation is mainly upheld from the “goods” side of the ledger, with food prices making a standout contribution. Trying to bring down food inflation with interest rate hikes is a suspect endeavor, because there isn’t much the ECB can do to cool demand.

With that in mind, tightening policy further at this stage would be mostly performative. Policymakers might reckon it a necessary step to burnish their inflation-fighting credentials, though how much that matters at this stage is unclear given the markets’ uninterested response to the latest repricing of expectations.

Euro may drop if the ECB opts to hold fire

Alternatively, the doves on the ECB Governing Council may prevail in keeping rates unchanged, reasoning that disinflation will happen on its own over time as growth sputters. Tightening the screws further when the economy is already flirting with recession seems unnecessary.

The euro looks troubled either way, but selling pressure may heat up in the latter scenario. Forcing a dovish about-face in expectations if ECB President Lagarde and company hold fire now that a rate hike has been fully discounted is likely to inspire sellers, threatening to push the currency back toward the 1.06 level against the greenback.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.