Global Recession is a Growing Risk

Global Recession is a Growing Risk

By:Ilya Spivak

China struggles while U.S. inflation data points to “higher for longer” Fed rate path

- Chinese PMI surveys to show the economy continued to deteriorate in August.

- U.S. PCE report seen echoing CPI data, showing inflation accelerated in July.

- Weak China, “higher for longer” Fed rates outlook boost global recession risk.

The world’s top two economies are diverging, and that’s bad news for global growth.

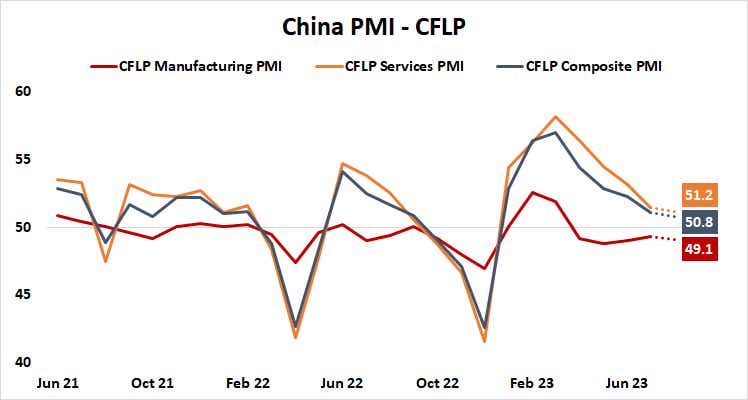

Purchasing managers index (PMI) data out of China is expected to show that economic activity growth continued to deteriorate for a fifth consecutive month in August. The manufacturing sector has been contracting since April and is projected to shrink further, according to a Bloomberg survey of economists.

The service sector is seen growing at the slowest pace so far this year, a telltale sign of the disappointment on display since Beijing opted to scrap “zero-COVID” restrictions in December 2022. An early burst of domestically driven growth powered by pent-up demand has seemingly fizzled, while overseas appetite has not returned to pre-pandemic levels.

Economic data outcomes have increasingly underperformed relative to consensus forecasts in recent months, according to figures from Citigroup. This suggests that analysts’ models are still rosier than they ought to be, implying scope for another set of surprises on the downside when the PMI numbers cross the wires.

PCE data expected to confirm U.S. inflation picked up in July

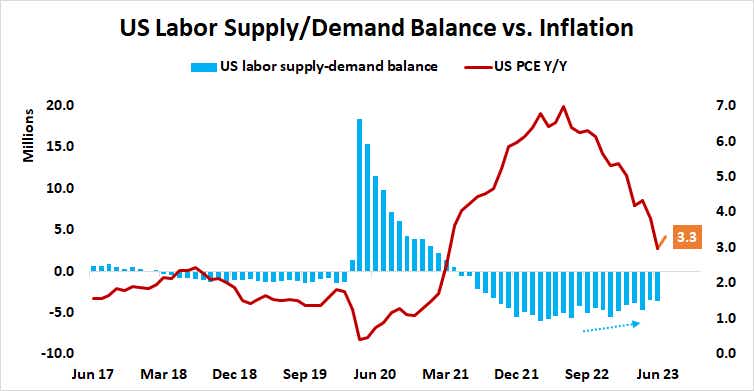

Meanwhile, July’s edition of the personal consumption expenditures (PCE) inflation measure–the Fed’s favored benchmark for price growth—is seen echoing consumer price index (CPI) numbers published earlier this month. They showed disinflation stalling, and PCE is expected to follow suit.

The service sector continues to be the culprit. Housing is the largest contributor to price growth, where Jerome Powell, chair of the Federal Reserve and company have relatively little agency to create near-term change. This is likely to keep the spotlight on the labor market, where a lingering post-pandemic disparity between supply and demand made inflationary wages sticky.

Some signs of cooling have started to emerge as recently as this week. Job Openings and Labor Turnover Survey (JOLTS) data this week showed that job openings fell by more than expected in July. Hiring data from ADP–a large payroll processing firm–undershot forecasts for August private sector employment growth by 18,000 jobs.

Still, analysts have penciled in a 3.5% unemployment rate to be reported in official August labor market statistics due out Friday. That’s just a hair above the 55-year low at 3.4% recorded in January (and matched in April). Federal Reserve officials have made a point of wanting to see this rise in earnest if they are to believe that disinflation will succeed.

Global recession risks are rising on weak China, inflation-minded Fed

This has driven markets to adjust priced-in policy expectations to a “higher for longer” interest rate path, even amid vigorous debate about the probability of another 25-basis-point (bps) rate hike this year. Fed Funds futures show the 12-months-forward outlook for the U.S. central bank’s target rate has moved from 3.6% to 5% since early May.

On balance, this means that the Fed is of a mind to cool U.S. growth further while China offers little by way of offset. Adding now nearly certain Eurozone recession to the mix makes global recession a clear and present risk in the near-term. Taken together, these three economies amount to over half of worldwide gross domestic product (GDP) growth, and that’s before considering that most of the rest are – in one way or another—vendors dependent on demand from one or more members of the trio.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.