Bonds’ Reversal Has Legs

Bonds’ Reversal Has Legs

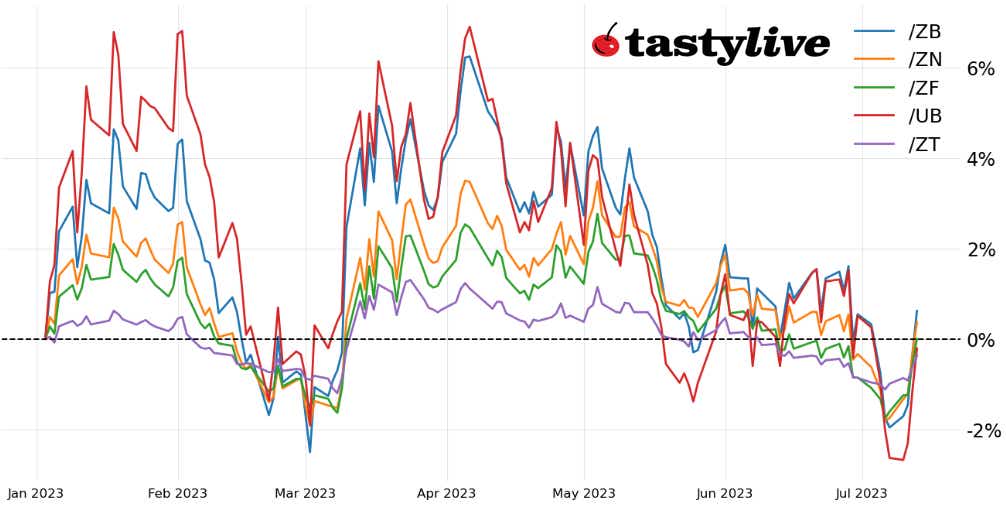

The recovery in /ZN this week is good news for stocks and precious metals—but bad news for the U.S. dollar.

- The bond market is telling us the Federal Reserve’s fight against inflation is wrapping up.

The drop in U.S. inflation rates may slow over the coming months, but the trajectory remains downward.

The bullish reversal in /ZN this week is good news for stocks and precious metals, and bad news for the U.S. dollar.

U.S. 10-year note up 2.28% from July low

The first few weeks of summer have proved interesting for U.S. Treasury bonds. The non-U.S. debt default at the start of June helped shift the focus back to the Federal Reserve’s efforts to tame inflation, and with the regional banking crisis seemingly quelled, traders began to price interest rates as if the Federal Open Market Committee (FOMC) would begin hiking rates back toward 6%.

Indeed, in early July’s illiquid, holiday trading conditions, a slew of data spooked those traders not vacationing on Lake Michigan or in the Hamptons, pushing U.S. Treasury yields up to their yearly highs. Yet something changed on Friday, July 7, when the June U.S. nonfarm payrolls report was released: Suddenly, the market responded as though the FOMC had the goal line of a soft landing in sight.

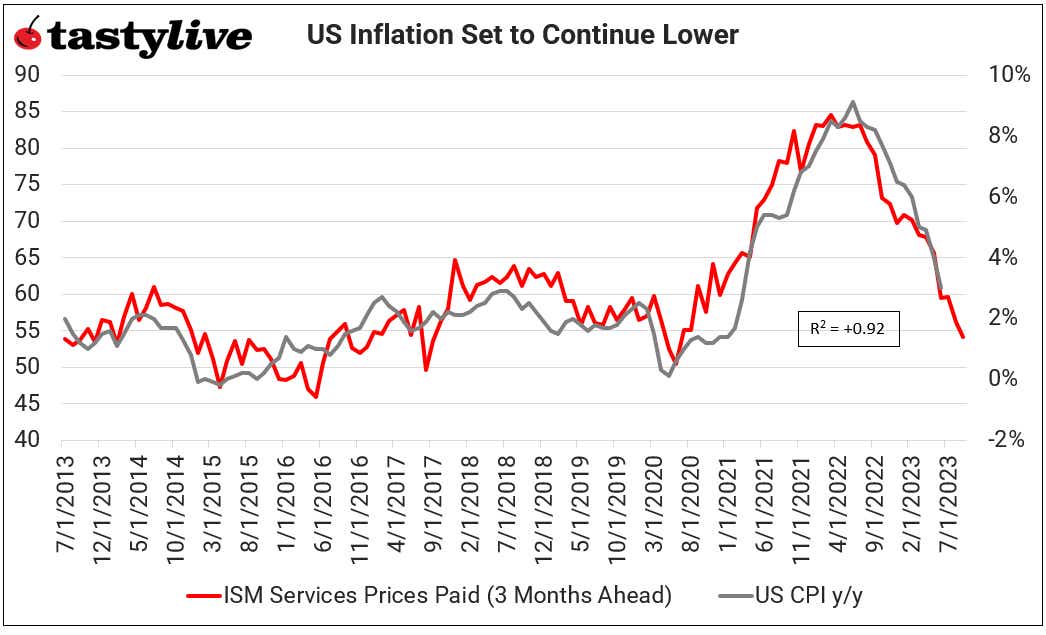

This trend—higher U.S. equity prices, higher U.S. bond prices and a weaker U.S. dollar—continued with fervor upon the release of the June U.S. inflation report on Tuesday, July 12. Producing the lowest headline U.S. inflation rate since March 2021, the June U.S. consumer price index (CPI) reading offered more evidence that price pressures are coming down, and in concert with other decent data, that inflation should continue trending lower.

One such chart to illustrate this point is a comparison of U.S. CPI year over year to the prices paid component of the Institute of Supply Management (ISM) services report. Over the past 10 years, these two data series have held a +0.92 correlation.

US CPI y/y versus ISM Prices Paid, Advanced: Monthly Chart (July 2013 to June 2023)

This is not a forecast by any means. Positive base effects within the CPI dataset suggest inflation won’t necessarily fall as fast over the coming months as it did in the first half of 2023, but it does illustrate the prevailing downward trend of price pressures over the next several months. The June U.S. producer price index, released Thursday, July 13, served as a hefty dose of confirmation bias for a market already leaning into the “inflation fight is over” camp.

/ZN U.S. 10-year note price technical analysis: daily chart (November 2022 to January 2023)

In the immediate wake of the June U.S. inflation report release, it was noted that “traders may find that their growing expectations of a less hawkish Fed will prove disappointed in the coming weeks. For now, however, the trend is your friend, and the trend is pointing to additional strength in stocks and a further retrenchment in U.S. yields.” Lower yields mean higher prices. This remains the case, and the technical picture reinforces the view that bond prices have a chance to rebound further.

Christopher Vecchio, CFA, tastylive’s head of futures and forex, has been trading for nearly 20 years. He has consulted with multi-national firms on FX hedging and lectured at Duke Law School on FX derivatives. Vecchio searches for high-convexity opportunities at the crossroads of macroeconomics and global politics. He hosts Futures Power Hour Monday-Friday and Let Me Explain on Tuesdays, and co-hosts Overtime, Monday-Thursday. @cvecchiofx

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.