U.S. Inflation: Stocks at Risk After PCE Data Hints at Only Modest Fed Rate Cuts

U.S. Inflation: Stocks at Risk After PCE Data Hints at Only Modest Fed Rate Cuts

By:Ilya Spivak

Stocks may be disappointed with U.S. PCE inflation data that sets the stage for Fed rate cuts but falls short of endorsing the markets’ aggressive easing expectations

- U.S. PCE inflation data is likely to set the stage for Fed interest rate cuts.

- Easing that helps clear the housing market might even help Fed efforts.

- Stocks may be disappointed with “slow and steady” PCE disinflation.

December’s update of the U.S. inflation gauge favored by the Federal Reserve is likely to set the stage for interest rate cuts in 2024.

The key question for financial markets is whether that remains a reason to push stocks higher and extend the blistering rally from November 2023.

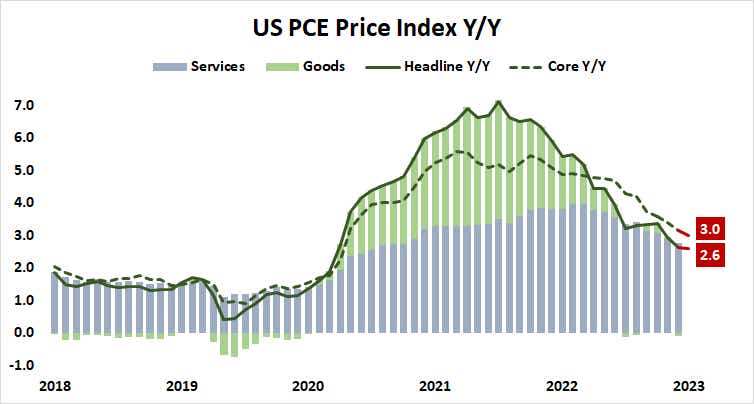

The headline personal consumption expenditure (PCE) price index is expected to have increased 2.6% year-on-year in December, keeping the inflation rate unchanged from the prior month. The more closely watched core gauge excluding food and energy costs is seen edging helpfully lower to 3%, marking the lowest reading since March 2021.

U.S. inflation: cooling where it matters most

Prices seem to be cooling for the right reasons. What’s left of sticky inflation is trapped in the “core services” part of the PCE basket, where an estimate of housing costs is doing the heavy lifting. The alternative consumer price index (CPI) inflation measure released earlier this month showed “shelter” prices driving core disinflation.

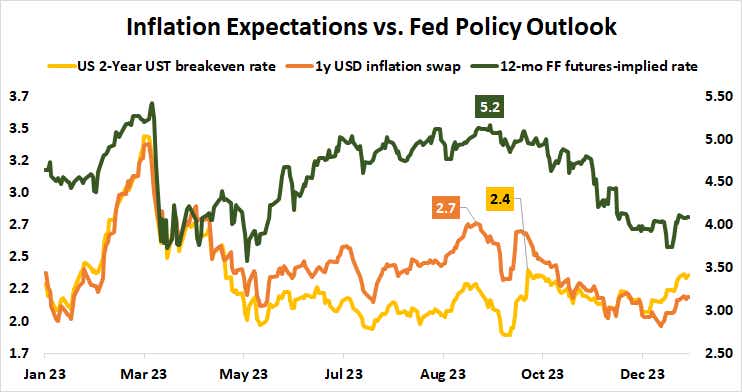

The Fed’s rapid rate hikes catapulted mortgage rates higher, driving both buyers and sellers out of the property market. The drop in turnover drove down inventories to historic lows, locking in elevated prices. Curiously, this means that building interest rate cut expectations might help bring inflation lower.

The gap between the market rate on a standard 30-year fixed rate mortgage that is nearly ubiquitous for U.S. borrowers and the average rate on outstanding mortgage debt has narrowed as the markets moved to price in a big-splash rate cut cycle in 2024. It was at a seven-month low by the end of 2023, down from a peak in late October.

Stocks and Fed interest rate cuts: searching for Goldilocks

Market-based measures of inflation expectations have tellingly fallen alongside the dovish adjustment in the Fed policy outlook in recent months. That seems to endorse the idea that—at worst—rate cuts will not undermine progress toward the central bank’s inflation goal. If market-clearing activity in housing is unlocked, they may help.

All this suggests that the PCE report is likely to encourage Fed Chair Jay Powell and the rate-setting Federal open Market Committee (FOMC) toward the start of easing. That may not cheer Wall Street nearly as much as it did in November and December, with markets more focused on the scale of easing rather than its eventuality.

Stocks struggled in the wake of January’s purchasing managers index (PMI) and fourth-quarter U.S. GDP data this week. Both showed unexpected strength. This hints that markets are displeased with the prospect of a more modest easing cycle. If the PCE report does little to counter such worries, sulking investors may push asset prices lower.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.