Macro Week Ahead: U.S. Inflation, Fed Chair Powell Speech, Chinese Economic Activity

Macro Week Ahead: U.S. Inflation, Fed Chair Powell Speech, Chinese Economic Activity

By:Ilya Spivak

Sentiment darkened last week as data undershot economists’ forecasts

- Stock markets are shuddering as consumer confidence data brings inflation red flag.

- U.S. CPI data and Fed Chair Powell speech come into focus as rate cut outlook evolves.

- Soft Chinese retail sales and industrial production data may bring fear of recession.

A quiet drift upward for most of the week seemed to hit a wall on Friday as U.S. consumer confidence data from the University of Michigan (UofM) spooked the markets. The data showed that sentiment darkened—undershooting economists’ forecasts by a wide margin—as the one-year inflation outlook jumped, as expected.

The UofM report signaled the Federal Reserve may be more reticent to cut interest rates this year than investors are hoping. The figures arrived just in time to set the stage for a busy week of releases shaping monetary policy expectations on the economic calendar in the days ahead.

Here are the macro waypoints likely to shape price action this week.

Federal Reserve Chair Powell speech

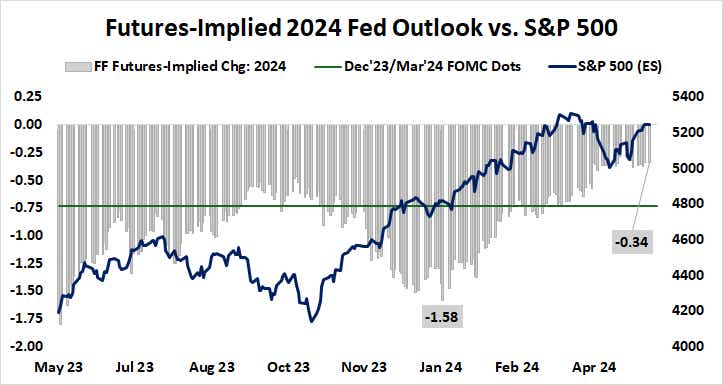

The U.S. central bank chief is scheduled to speak at the annual meeting of the Foreign Bankers’ Association in Amsterdam. Traders will be looking for any language signaling that worries about sticky inflation are undercutting the Fed’s confidence in delivering stimulus this year.

As it stands, the markets are pricing in 34 basis points (bps) in cuts this year. That amounts to one standard-sized 25bps rate cut and a 36% probability of a second one.

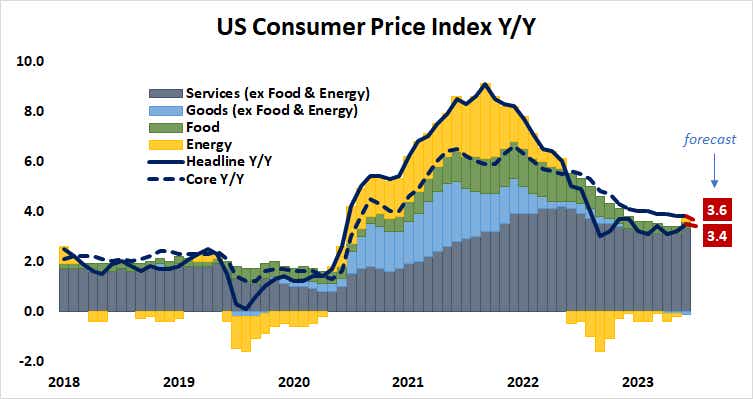

U.S. consumer price index (CPI) data

U.S. inflation is expected to have cooled in April. The headline price growth rate is seen falling to 3.4% year-on-year, retreating from the six-month high of 3.5% set in March. The core measure excluding volatile food and energy prices edges down to 3.6%, the lowest in three years.

An upside surprise on the headline figure may be in the cards. Rising crude oil prices since the beginning of the year have entered the CPI calculation with about a one-month lag. The WTI benchmark slipped last month but the March rise is yet to be accounted for.

Another hotter-than-expected inflation number may spook stock markets as traders even if the core measure – the one most emphasized by Fed officials—mostly meets expectations. The markets’ elevated sensitivity to anything that might extend the “higher for longer” narrative on interest rates might trigger a broadly risk-off reaction.

China industrial production & retail sales data

Chinese economic activity figures are expected to show improvement in April, with retail sales and industrial production quickening from the previous month. Analytics from Citigroup suggest China’s economic data outcomes have been deteriorating relative to forecasts recently, setting the stage for disappointment.

Soft results might revive worries about a global economic downturn, especially in the wake of a month of softening U.S. data outcomes. Stock markets might wobble if talk of recession re-emerges.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.