Stocks, Bonds and the Dollar Hang in the Balance on U.S. Jobs Data

Stocks, Bonds and the Dollar Hang in the Balance on U.S. Jobs Data

By:Ilya Spivak

Their fate hinges on how many Fed interest rate cuts seem possible after the release of the employment figures

- All eyes are on the March U.S. jobs report after a macro-heavy week.

- Wage data is in focus amid a loud debate about the path of inflation.

- Stocks, bonds and the U.S. dollar hinge on how Fed rate cuts evolve.

Financial markets are gearing up for the crescendo after a week of big-splash macro event risk: the March U.S. employment report from the Bureau of Labor Statistics (BLS). Traders will parse the data for clues about next steps for the economy and Federal Reserve monetary policy.

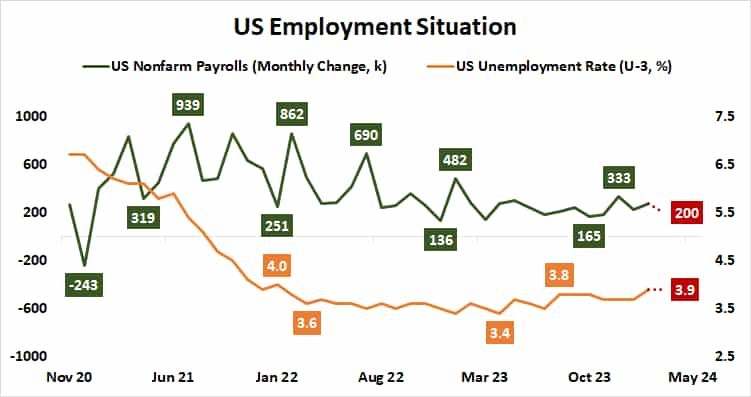

Consensus forecasts envision a rise of 200,000 in nonfarm payrolls, marking a slight downswing from the 275,000 increase recorded in February. The unemployment rate is seen holding steady at 3.9%, a two-year high. Average hourly earnings growth—a measure of wage inflation—is seen cooling to 4.1% year-on-year from 4.3% in February.

Wages in focus as key labor market data looms

A payrolls number that prints broadly in line with expectations would amount to an extension of familiar trends. The 12-, six- and three-month averages for monthly U.S. jobs growth range from 232,000 to 279,000. Absent a shocking surprise, the jobless rate would be likewise unremarkable. It has sat in 3.4%-4% range since January 2022.

The wages component might be the most interesting bit of the bunch. Squeezing inflation out of the labor market is front and center for Fed policymakers as they continue to argue that interest rate cuts are probably on the menu for this year. If pay growth fails to cooperate, the markets might wobble as stimulus prospects weaken.

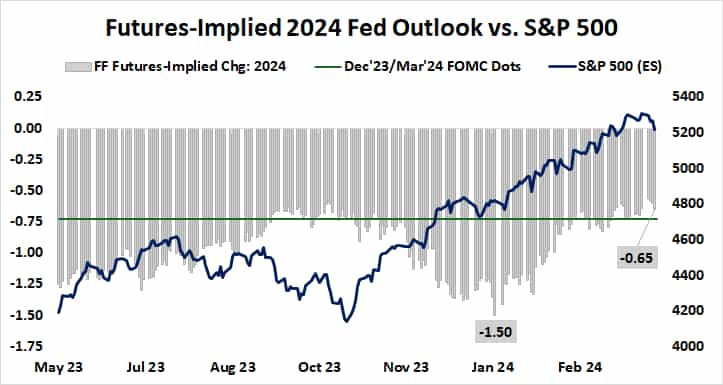

Analytics from Citigroup reveal that U.S. economic data outcomes have been strengthening relative to baseline forecasts since mid-March. That has pushed the markets to scale back expectations for interest rate cuts. Fed Funds futures are pricing in 65 basis points (bps) in easing this year. That’s two standard 25bps reductions and 60% of a third one.

For its part, the Fed stuck with a forecast calling for three cuts when it published the latest Summary of Economic Projections last month. Speaking this week, Fed Chair Jerome Powell called current policy “tight” and warned that it is too soon to tell if the recent pickup in price growth is anything more than a bump in the road toward disinflation.

How many Fed rate cuts will the U.S. jobs report allow?

The markets got a glimpse of what weakening growth and inflation might look like with stunningly weak service-sector data earlier this week from the Institute of Supply Management (ISM). It showed the slowest expansion in three months, a second month of shrinking employment and price growth at its weakest since March 2020, the low set amid the onset of the COVID-19 pandemic.

On balance, a jobs report that leaves the markets thinking steady growth and sticky inflation will force the central bank to push back its rate cut intentions seems likely to weigh on stocks and bonds alike. The U.S. dollar is likely to power higher against most of its peers in this scenario. An echo of the soggy ISM data stands to yield the opposite results.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.