Stock Market at Risk as Rate Cut Expectations Cool and China Struggles

Stock Market at Risk as Rate Cut Expectations Cool and China Struggles

By:Ilya Spivak

Stocks and bonds may continue to suffer as the U.S. dollar rebounds amid cooling Fed rate cut bets. U.K. inflation data may likewise push back on stimulus hopes, but weakness in China still threatens global growth.

- Fear of global recession may resurface if economic data from China disappoints.

- The British pound may get a lift if U.K. inflation data cools rate cut speculation.

- Steady U.S. retail sales growth may challenge dovish Fed policy expectations.

Another holiday-shortened week for U.S. financial markets has opened with a wave of skepticism about the priced-in expectations for Federal Reserve monetary policy. Stocks fell alongside bonds as yields pushed higher. The U.S. dollar drove higher against its major counterparts and gold prices fell.

A unifying pattern screams to be seen. Indeed, rate cut expectations priced into Fed Funds futures have visibly cooled. Nevertheless, traders still anticipate six 25-basis-point (bps) reductions are on the menu this year. The first cut is seen appearing no later than May. The probability of a sooner move in March is at a hefty 66.8%.

The markets will have to contend with a dense economic calendar from here.

Chinese economic activity data

Analysts expect to see economic growth accelerated in the world’s second-largest economy in the fourth quarter of 2023. China is due to report gross domestic product (GDP) grew 5.3% year-on-year, topping the 4.9% increase in the three months to September.

Parallel releases are set to show industrial production grew 6.6% year-on-year in December, matching November’s pace. Meanwhile, retail sales growth slowed to 8% over the same period, cooling after the prior month’s jump of 10.1%. The jobless rate is penciled in at 5% for the fourth consecutive month.

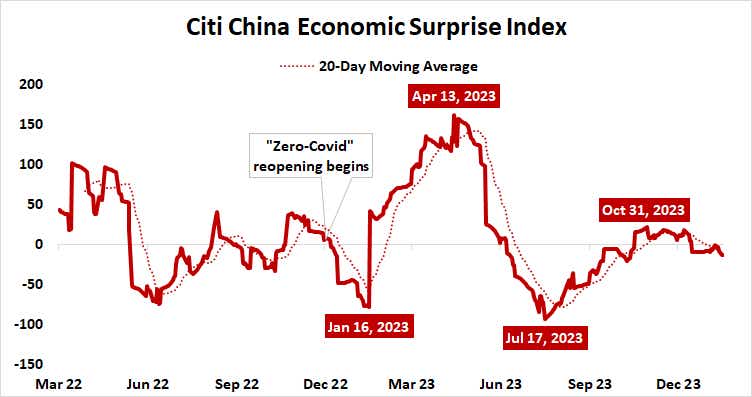

Analytics from Citigroup suggest realized outcomes for Chinese economic releases are cautiously drifting away in a disappointing direction relative to baseline forecasts over recent months. If that proves to set the stage for downside surprises, fears of a global slowdown may keep stocks pressured even as bonds rebound and yields come in.

U.K. consumer price index (CPI)

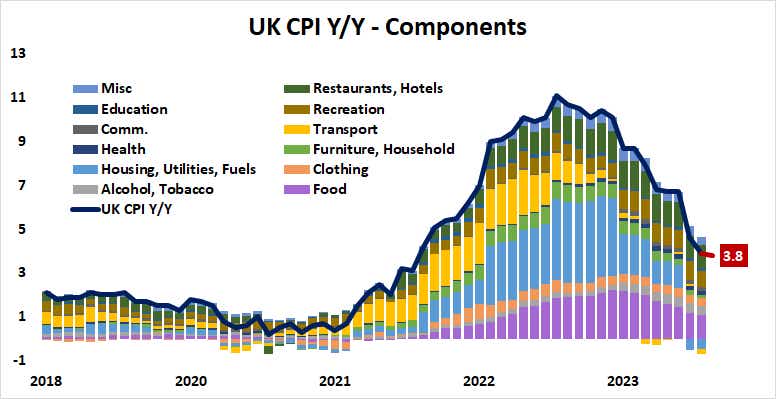

Inflation in the UK is seen cooling in December. A rise of 3.8% year-on-year in the consumer price index (CPI) is expected, marking the lowest reading since September 2021. Traders will look for the outcome to offer a view on broader monetary policy trends as most global central banks gear up to join the Fed in cutting back borrowing costs.

Food prices remained the biggest contributor to price growth in November. Bank of England (BOE) policy has relatively little influence here, and pressure appears to be receding by itself. The other pillars of price growth—recreation and hospitality—are helpfully amenable to cyclical coercion, however, and ought to ease as economic activity slows.

Leading purchasing managers’ index (PMI) data suggests U.K. economic activity returned growth and even accelerated over the past two months, powered by a resurgent service sector. BOE rate-cut expectations might adjust to a more modest setting if this buoyancy echoes in the CPI data, boosting the British pound.

U.S. retail sales

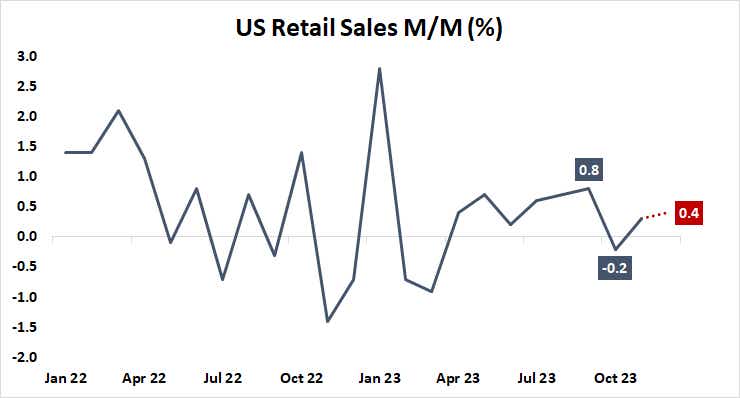

A familiar story is expected from the U.S. consumer in December. Receipts are seen rising recording a monthly rise of 0.4% in December, marking a slight pickup from November’s 0.3% increase. That would put the pace of sales growth firmly in line with quarterly, half-year and 12-month trend averages.

Citigroup data suggests that expected and realized results on U.S. economic data flow have converged in recent weeks, suggesting that outcomes are unlikely to stray too far from baseline forecasts. The key question posed by middling figures is whether the Fed will truly cut rates as swiftly as expected absent signs of acute economic pain.

If markets conclude current pricing is indeed excessive, a readjustment of the baseline toward expectations of a more modest easing effort may add fuel to the moves already underway at the start of the trading week. That bodes ill for stocks, bonds and precious metals, while the U.S. dollar may continue to press upward.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2024 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.